As part of our investment focus on each of the assets in the Stockspot portfolios, we look at why fixed interest, also known as bonds, forms an integral part of our portfolios.

What are bonds?

A bond is a piece of debt sold to investors usually by a company or the government. Bondholders “lend” money to the bond issuer for an agreed period (until “maturity”) and in return for that, they are paid a regular income in the form of interest.

Investors in bonds can earn a return in 2 ways:

-

From the income received through the bond interest payments.

-

By selling the bond. If you hold a bond to maturity, you will get face value of the bond back, which is usually $100. However it is possible get more (or less) back by selling a bond before it matures. This is because bonds, like shares, trade on a secondary market and their prices are always changing.

What are bond ETFs?

Similar to Exchange Traded Funds (ETFs) for shares, bond ETFs include a portfolio of many bonds which track an index. The most commonly used bond index in Australia is the Bloomberg AusBondComposite Index (former UBS Composite Bond Index). This index invests in investment-grade bonds issued by Australian Treasury, state governments and companies.

In our Australian ETF Report we profiled the 15 different bond ETFs listed on the ASX. Since we published the report, several new bond ETFs have listed, including a few that invest in international bonds to give Australian bond investors global diversification.

| New bond ETFs (since March 2019) | Invests in |

| BetaShares Australian Government Bond ETF (AGVT) | Investment grade corporate fixed bonds issued by Australian federal and state governments, and supranational and sovereign agencies. |

| BetaShares Sustainability leaders Diversified Bond ETF – Currency Hedged (GBND) | Corporate and government bonds with a specific focus on green bonds (for environmental projects such as renewable energy and pollution prevention) and corporate bonds that are not involved in activities such as mining and fossil fuels. |

| VanEck Vectors Australian Subordinated Debt ETF (SUBD) | Investment grade floating rate subordinated debt. This is similar to traditional bonds, but are instead unsecured loans that rank below senior loans. If a borrower were to default, subordinated debt holders will only be paid once all other corporate debts are settled. |

| VanEck Vectors Emerging Income Opportunities Active ETF (Managed Fund) (EBND) | An actively managed fund that invests in a diversified portfolio of emerging market bonds from countries such as Indonesia, Thailand, and Argentina. |

Currently the Stockspot portfolios invest in the iShares Composite Bond ETF (IAF) which tracks the Bloomberg AusBond Composite 0+Yr Index. We believe that this ETF offers a good mix of Australian government, semi-government and company bonds. You can read more on our review on the best Australian bond ETFs.

In addition, its relatively short average bond payback period of 5.5 years (also known as duration) reduces our clients’ exposure to long-term interest rate changes – as we will discuss below.

What causes bonds to rise or fall in value?

There are a few factors that influence bond prices between when they are issued and when they mature. The 2 most influential factors are changes in interest rates and credit risk.

Changes in interest rates

Bonds are an alternative to leaving your money in the bank, so as interest rates rise investors demand higher returns, and demand for bonds falls. On the other hand, falling interest rates cause bonds to rise.

The longer-dated bonds are, the more sensitive they are to interest rate changes since any changes compound over many years. This is why we prefer shorter-dated bonds for our clients to reduce the impact of any changes in long-term interest rates.

Bonds that have already been issued and are trading must continually re-adjust their prices and yields to stay in line with current interest rates. When interest rates fall, as they have been in Australia over the past couple of years, investors can benefit from capital appreciation in addition to interest.

In 2019, IAF returned 7.2% which was made up of a 2.3% coupon (interest) and 4.9% capital gain as interest rates fell in Australia. Bond prices move inversely to interest rates, so when rates fall, bond prices tend to rise.

Many central banks across the world have been re-introducing quantitative easing (QE) policies to combat slowing economic acticity due to the coronavirus outbreak. QE generally refers to when central banks buy government bonds in the market. This puts downward pressure on rates, makes it cheaper for businesses to borrow money, encourages consumer spending and has a positive wealth effect for all asset holders.

Creditworthiness

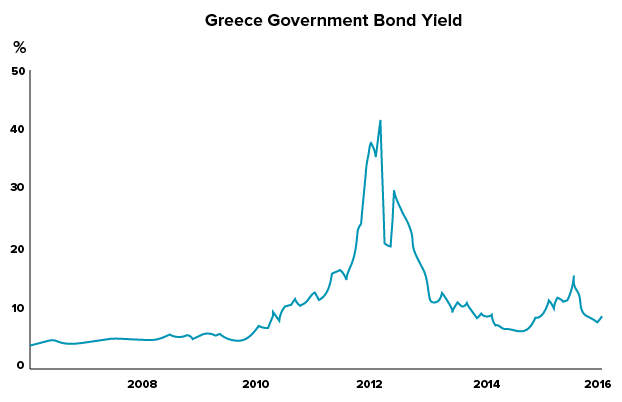

Credit risk also contributes to a bond’s price since it influences the likelihood of a company being able to pay back bondholders. When companies (or governments) are facing financial struggles or take on a lot of debt, their bond prices often fall to reflect the higher possibility of the company (or government) going bust.

During the Greek financial crisis, Greek bond yields rose to 46.8%. This means investors were so concerned with Greece’s ability to pay back debt that they required a 46.8% return to compensate for that risk.

In general however, bonds tend to be less risky than shares since they have a set repayment date and repayment amount. Also, in the event of the company being liquidated, bondholders are paid before shareholders.

How do bonds compliment shares?

Bonds and shares work together well in a portfolio for a few key reasons:

Diversification

Bonds are counter-cyclical. That means when the economy is in recession and interest rates are falling, bond prices tend to rise. On the other hand, when the economy is expanding or at its peak, bonds become less attractive.

Bonds usually move in the opposite direction to shares, which is why they often described as a defensive asset. We can see in the chart below, bond returns have tended to be positive when returns on shares have been negative. It is this movement in opposite directions that help to smooth the ups and downs in an overall portfolio.

Income

Most of the investment return from bonds comes in the form of interest income. Since Bond ETFs include broad portfolio of bonds, these interest payments provide a reliable stream of income. The chart below shows that unlike shares, which have historically focused on capital returns, bond returns have largely come from interest income.

A note on cash

We sometimes get asked why we include bond ETFs in our portfolios and not cash. Cash and term deposits can be better described as savings instruments rather than an investment.

They are better used for paying short term expenses or meeting near term financial goals. This is why we encourage of all of clients to keep enough cash and short term deposits to be able cover their immediate cash needs (usually 3-6 months of expenses).

Cash and term deposits offer relatively low interest since they don’t carry much risk. In contrast, bonds will offer higher expected returns over the long term for investors willing to take on slightly more risk.

These higher returns are compensation for investors taking on higher amounts of interest rate and credit exposure. Therefore bonds generally suit an investor with a longer investment time horizon.

Why bonds belong in your portfolio

By combining shares and bonds in a portfolio, investors are able to better manage their risk to generate predictable long-term returns. In his 2014 investors letter to shareholders, famed investor Warren Buffett said:

My advice [to my trustee] could not be more simple… put 10% in short-term government bonds and 90% in a very low cost [S&P 500] index fund. I believe the long term results from this policy will be superior to those attained by most investors… whether pension funds, institutions or individuals.

Warren Buffett

Just as Buffett has described, share and bond ETFs form the building blocks of our portfolios. We aim to combine them in a way that gives our clients the best chance of reaching their goals.

For clients with a shorter investment horizon this typically means more bonds, and for those like Buffett, with a long time-frame, they can afford to invest a majority in shares.

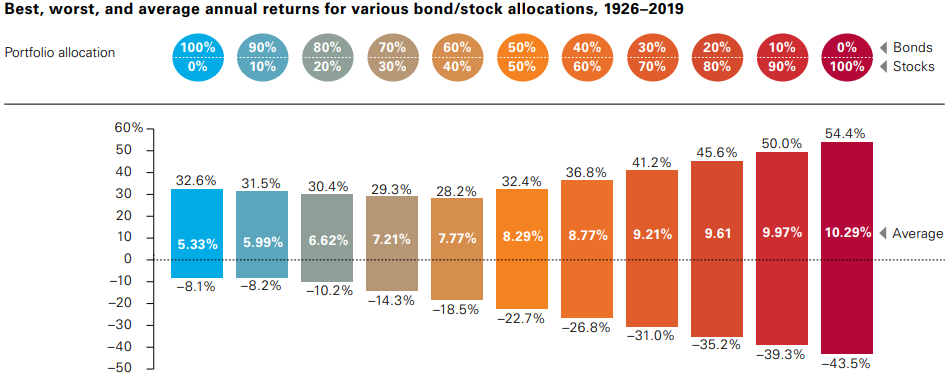

This chart shows the best, worst and average annual returns between 1926 and 2019 based on different combinations of bonds and shares in the US. As you can see, the higher your allocation to shares (red side), the better your average long-term returns would have been, but with more down years along the way.

On the other hand, by focusing a portfolio in bonds (blue side), investors could reduce the chance of down years, at the cost of lower returns.

By finding out about our clients’ investment horizon, risk propensity and cashflow needs, we’re able to recommend the ideal combination of shares and bonds to suit their personal goals.

Find out how Stockspot makes it easy to grow your wealth and invest in your future.