Australian Bond ETFs are often one of the most overlooked asset classes on the ASX, yet they deserve a starring role in every balanced portfolio. When share markets are “shaken, not stirred,” bonds can provide the steady income and stability investors crave.

In this blog we review the best performing Australian bond ETFs of 2025 to help you enter 2026 empowered. We explain how bond ETFs can help diversify your portfolio, reduce risk, and generate reliable returns. You’ll learn what fixed income bonds are, how they work, and how the ETFs rank this year on factors like size, liquidity and performance track record.

Historically, only around 6% of Australian investors have owned bonds, compared to 60% who hold shares, (according to the 2023 ASX Australian investor study), but with the growth of bond ETFs it’s now easier than ever to access diversified fixed income exposure via bond ETFs.

What are fixed income bonds?

A bond (also known as fixed income) is a loan made by investors to a company or government.

Bondholders lend money to the bond issuer for an agreed period (until maturity) and in return for that, they are paid a regular income in the form of interest. At the end of the agreed period, investors also receive their principal back.

Historically, bonds haven’t made it into most people’s portfolios, with Australian investors preferring to invest in the share market, but bonds have the benefit of offering a cushion to investors when share markets fall. This is why we think bonds belong in every investor’s portfolio.

Bonds are considered by many to be boring, but at Stockspot, we believe that boring is brilliant.

Until recently, it has been difficult for everyday investors to access bonds due to high minimum investment amounts, lack of diversification and costs.

However, with the rise of Exchange Traded Funds (ETFs), Australian investors now have a solution to easily access bonds and make them a part of their portfolios.

The growth of Australian bond ETFs

Australian Bond ETFs enjoyed strong growth over the last 6 years, growing almost 338% from $8b in 2019 to $35b in December 2025 (source: ASX).

Despite rapid growth between 2017 and 2022 (growing over 607% in the 5 year period), their growth has slowed over the past few years, due to rising interest rates resulting in bonds posting poor returns.

As interest rates began to fall in 2025, and amongst wider market volatility bond ETFs have seen an uptick in growth, growing by almost 35% between December 2024 and December 2025. Increasing market volatility in 2026 is seeing investors continue to invest money in Australian bond ETFs.

We believe this will continue, as ETF issuers release more Australian bond ETFs and investors demand more defensive assets to smooth out the returns from investing in shares.

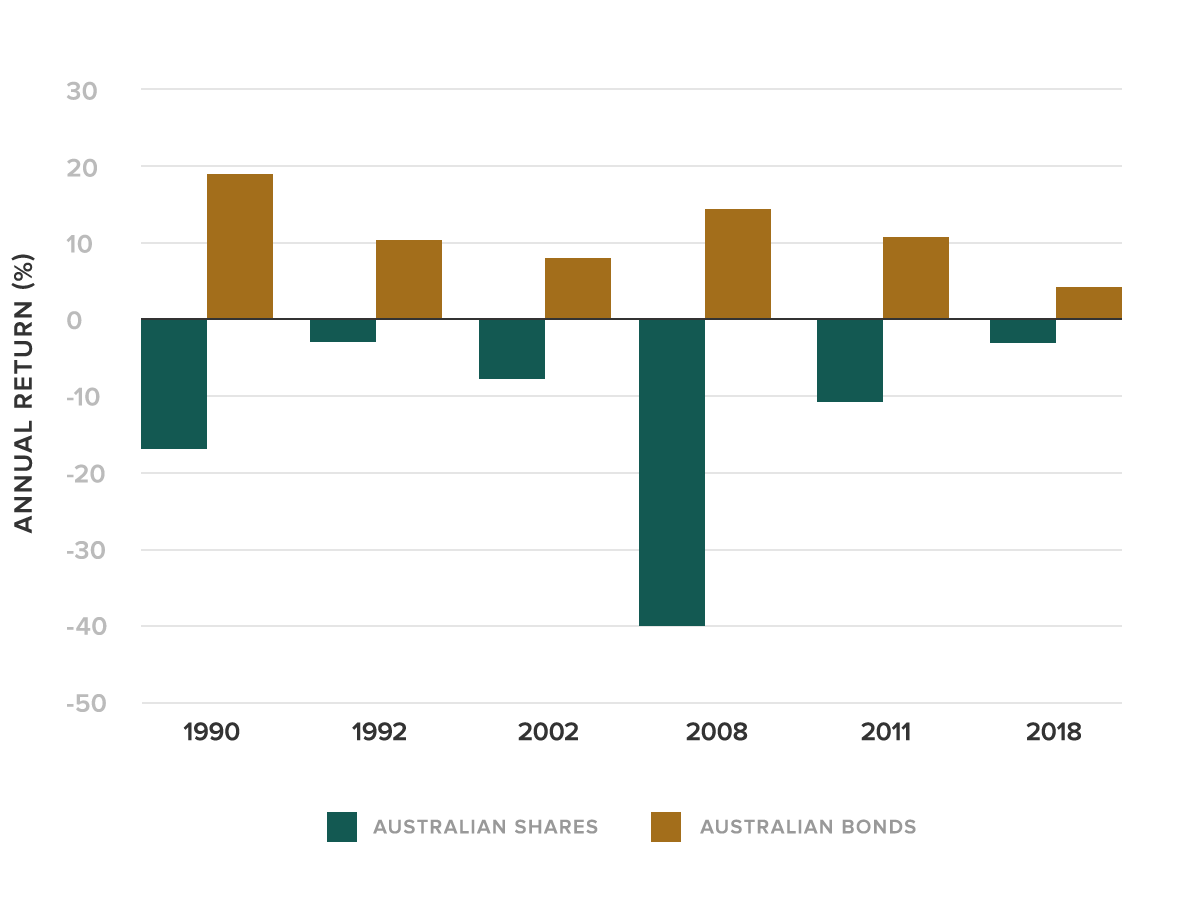

Taking a long lens over the last 30 years, it is clear that when shares fall, high grade bonds do their job as a portfolio cushion and rise.

Australian bonds were one of the few asset classes with a positive return in 2018, for example, when share markets fell. Bonds were also the ballast that helped cushion the fall during the COVID-19 share market fall.

What are the advantages of Australian bond ETFs vs buying individual bonds or shares?

- Diversification: Bond ETFs hold a basket of bonds which improves overall portfolio diversification and reduces the chance of you lending a large amount to a dud company.

- Transparent pricing: Bond ETFs are tradeable on the ASX whereas most individual bonds trade in more complex markets with pricing that is not very transparent and incurs higher costs when getting in and out.

- Performance: Bond ETFs track time-tested indexes, which continually do better than active bond fund managers. The SPIVA Mid-Year 2024 Highlights report showed that, over the past 10 years, 70% of active Australian Bond managers underperformed the index benchmark.

- Yield: Bonds can provide regular, consistent and predictable income, with less volatility than shares, potentially adding another income stream beyond share dividends.

Compare Australian bond ETFs

Following the success of our Australian ETF Report, we will road test some of the most popular Australian Bond ETFs to help you decide, which is the best Australian bond ETF for your portfolio:

- iShares Core Composite Bond ETF (IAF)

- SPDR S&P/ASX Australian Bond Fund (BOND)

- Vanguard Australian Fixed Interest Index ETF (VAF)

- Vanguard Australian Government Bond Index ETF (VGB)

- BetaShares Australian Government Bond ETF (AGVT)

- iShares 15+ Year Australian Government Bond ETF (ALTB)

- VanEck 5-10 Year Australian Government Bond ETF (5GOV)

We compare them across 5 factors:

What is the biggest Australian bond ETF?

The largest Australian bond ETFs by funds under management are iShares Core Composite Bond ETF (IAF) and Vanguard Australian Fixed Interest ETF (VAF). IAF manages about $3.62 billion, while VAF oversees roughly $3.45 billion, making them the clear market leaders.

Vanguard Australian Government Bond ETF (VGB) has accumulated around $1.33 billion since it launched in April 2012, while BetaShares Australian Government Treasury ETF (AGVT) has grown to approximately $1.13 billion since it launched in July 2019.

The smallest of the bond ETFs are 5GOV (~$91 million) and BOND, the smallest Australian bond ETF, with just $39 million in assets. Its slower growth is often attributed to higher fees, lower liquidity, and narrower diversification (about 160 holdings). BOND also follows a less widely recognised benchmark, which may reduce investor demand compared with larger, more established peers.

What is the cheapest Australian bond ETF to own?

When it comes to cost, investors pay attention to the headline management fee (known as the Management Expense Ratio [MER]), but this is not the only overhead.

Unfortunately, some ETF and Fund Managers bury hidden costs in their Product Disclosure Statements.

We also like to examine the slippage (buy/sell spreads) of each of the ETFs. This refers to how much you lose when buying/selling the ETF.

It is calculated as the average percentage difference between the best buyer and seller during market hours.

| ASX Code | Cost (MER) | Buy/Sell Spreads (aka slippage) |

| IAF | 0.10% | 0.03% |

| BOND | 0.10% | 0.10% |

| VAF | 0.10% | 0.05% |

| VGB | 0.16% | 0.05% |

| AGVT | 0.22% | 0.06% |

| ALTB | 0.15% | 0.13% |

| 5GOV | 0.22% | 0.08% |

The cheapest Australian bond ETFs on headline fees are IAF, BOND and VAF, each with a management expense ratio (MER) of 0.10%.

In Q2 2025, the SPDR S&P/ASX Australian Bond ETF (BOND) cut its fee from 0.24% to 0.10%, bringing it into line with market leaders IAF and VAF and improving its competitiveness on price.

But the MER is only part of the story. Investors should also factor in buy/sell spreads (slippage) — the average difference between the best buyer and seller on the ASX during trading hours. Spreads represent a real trading cost and can materially change the total cost of ownership.

IAF typically shows the tightest spreads at 0.03%, followed by VAF and VGB (0.05%). Despite its fee reduction, BOND’s spread is wider at about 0.10%, meaning trading costs can be more than three times higher than IAF. This is often linked to lower liquidity and a more concentrated portfolio.

Interesting market note: During the COVID-19 pandemic, Bond ETFs had their spreads widen due to market volatility. Importantly, this was not due to the ETFs but due to the illiquid pricing nature of the underlying bonds themselves.

History of bond ETF costs

2020- 2021

BlackRock reduced fees for its iShares Core Composite Bond ETF (ASX: IAF) from 0.20% to 0.15% in April 2020 and was the cheapest Australian bond ETF on the ASX, until VAF followed suit in October 2021, reducing its fee down from 0.20% to 0.15%.

2023

BlackRock further announced in February 2023 the move to reduce IAF’s fee down to 0.10% to reclaim the title of cheapest Australian bond ETF, until VAF matched it at 0.10% in April 2023.

2025

BOND was one of the more expensive ETFs charging 0.24% per year and with the largest slippage, it is the most expensive bond ETF to own. However in 2025 BOND reduced its fees to 0.10% to remain competitive with the likes of IAF and VAF.

What is the most liquid Australian bond ETF?

Australian bond ETFs have 2 layers of liquidity:

- the liquidity of the ETF

- the liquidity of the underlying bonds within that ETF

One measure of liquidity is measured by the average daily volume on the ASX. Volume is a measure of market making activity and trading interest which makes it a reasonable estimate of liquidity.

IAF is currently the most liquid Australian bond ETF, trading over $14 million per day, overtaking VAF, which trades just over $5 million per day. The next most liquid bond ETFs include VGB ($4.9 million) and AGVT ($3.9 million).

At the smaller end of the market, BOND trades only around $170,000 per day, while 5GOV averages roughly $416,000, which can contribute to wider spreads compared with the larger more liquid funds.

Greater trading volumes make it easier to buy and sell an ETF and reduce the spread/slippage involved.

Performance track record

| ASX Code | 1 Year Total Return | 3 Year Total Return (p.a.) | 5 Year Total Return (p.a.) |

| IAF | 1.3% | 2.0% | 0.0% |

| BOND | 1.9% | 2.0% | -0.1% |

| VAF | 1.4% | 2.0% | 0.1% |

| VGB | 1.1% | 1.5% | -0.3% |

| AGVT | 0.8% | 1.2% | -1.1% |

| ALTB | -1.2% | N/A | N/A |

| 5GOV | 0.7% | N/A | N/A |

What are the historic returns of Australian bond ETFs?

IAF, BOND and VAF continue to show broadly similar outcomes across the 1, 3, and 5-year periods. Over one year, BOND sits slightly ahead (1.9%) relative to VAF (1.4%) and IAF (1.3%). Over three years, all three (IAF, BOND and VAF) returned 2.0% p.a. Across five years the gap narrows, with BOND at -0.1% p.a., IAF at -0.0% and VAF at +0.1%. The closeness in results reflects that these ETFs provide exposure to broadly comparable mixes of Australian investment-grade bonds.

AGVT, which only recently moved beyond its five-year history (having launched in 2019), has delivered a 3-year return of 1.2% p.a. and a 5-year return of -1.1% p.a. underperformed over the 5 year period due to its longer duration of bond holdings (which was impacted by rising interest rates).

Given the performance of the funds are likely to be similar, we place a greater importance on other factors when assessing Australian bond ETFs. A longer track record for both the ETF and its underlying index can provide better insight into how the strategy behaves across varying market conditions and how reliably the fund follows its benchmark.Also important is the ‘tracking difference’ which measures how well an ETF does at mirroring its index.

Index changes:

In 2025 BOND changed its index benchmark. The index was reflective of returns from the S&P/ASX Australian Fixed Interest Index from fund inception until 19/06/2025 before changing to the S&P/ASX iBoxx Australian Fixed Interest Diversified 0+ Index effective 20 June 2025.

| ASX Code | Index | Index History (Inception Date) | ETF History (Inception Date) |

| IAF | Bloomberg AusBond Composite 0+Yr Index | September 1989* | March 2012 |

| BOND | S&P/ASX iBoxx Australian Fixed Interest Diversified 0+ Index | May 2025 | July 2012 |

| VAF | Bloomberg AusBond Composite 0+Yr Index | September 1989* | October 2012 |

| VGB | Bloomberg AusBond Govt 0+ Yr Index | December 2008 | April 2012 |

| AGVT | Solactive Australian Government 7 – 12 Year AUD TR Index | December 2007 | July 2019 |

| ALTB | Bloomberg AusBond Govt 15+ Yr Index | March 2021 | June 2024 |

| 5GOV | S&P/ASX iBoxx Australian & State Governments 5-10 Index. | December 2013 | September 2023 |

| ASX CODE | 5 YEAR ETF PERFORMANCE (P.A.) | 5 YEAR INDEX PERFORMANCE (P.A.) | TRACKING DIFFERENCE |

| IAF | 0.03% | 0.15% | -0.12% |

| BOND | -0.22% | 0.01% | -0.23% |

| VAF | 0.17% | 0.15% | 0.02% |

| VGB | -0.14% | -0.17% | 0.03% |

| AGVT | -1.14% | -0.95% | -0.19% |

| ALTB | N/A | N/A | N/A |

| 5GOV | N/A | N/A | N/A |

IAF has the longest track record (albeit marginally), having been listed for over 10 years, and tracks the widely used Bloomberg AusBond Composite Index. AGVT has only recently gained a 5 year track record and has a wider tracking difference.

Other factors

We look at a few other factors when selecting a bond ETF:

- Duration – This is a measure of how sensitive a bond is to changes in interest rates. Bond prices and interest rates have an inverse relationship (i.e. when interest rates go up, bond prices fall).

- Credit Quality – this is a measure of how likely a bond is to default (not pay its investors back). The scale ranges from the highest quality (AAA) to the lowest (D), with a rating of BBB- considered to be ‘non-investment grade’ and more risky. For example, Australia has a rating of AAA whereas a country like Mozambique is rated D. The lower the credit quality, the higher the risk of defaulting. Bonds with worse credit quality tend to pay a higher interest rate to compensate investors for taking more risk.

- Yield to Maturity – The rate of return an investor can expect if they hold the bonds until their maturity date. This does not factor in the price return, only the income return (known as coupon payments).

Bonds with shorter durations and better credit qualities provide a better diversification cushion when share markets fall. Poorer credit quality bonds can give you a higher yield but have a more similar correlation to shares so aren’t as helpful as a portfolio diversifier.

| ASX Code | Average weighted Maturity | Weighted Average Yield to Maturity |

| IAF | 5.8 | 5.1% |

| BOND | 6.0 | 5.4% |

| VAF | 5.8 | 5.0% |

| VGB | 6.4 | 5.0% |

| AGVT | 8.9 | 5.4% |

| ALTB | 21.4 | 5.5% |

| 5GOV | 7.4 | 5.1% |

Stockspot’s verdict on Australian bond ETFs

We selected IAF for the Stockspot portfolios due to its size, liquidity, track record, high credit quality and relatively short duration.

It is an effective diversifier for our Stockspot portfolios due to its ability to cushion against share market volatility.

Thanks to owning IAF and GOLD, Stockspot portfolios have delivered strong returns despite the 2020 share market downfall as a result of the coronavirus and market volatility as a result of wider global political events.

We also offer international bonds using the Vanguard International Fixed Interest Index (Hedged) ETF (ASX: VIF) as part of our Stockspot Themes range.

VIF invests in a diversified range of high credit quality and income generating bonds issued by governments around the world (such as the USA, Japan, France and the UK).

Other bond themes that Stockspot offers include the Vanguard Australian Corporate Fixed Interest Index ETF (ASX: VACF) and iShares Government Inflation ETF (ASX: ILB).