Every year, super funds annual performance. This article looks at how the funds twist their performance relative to other funds and indexing, and how they make their returns look better than they really are.

The funds’ PR is parroted by the ratings agencies whose tables and good news story are accepted at face value by the media.

Firstly, we look at how funds manipulate their inclusion into the categories set by the ratings agencies.

Defensive assets

ASIC defines defensive assets as cash or government bonds.

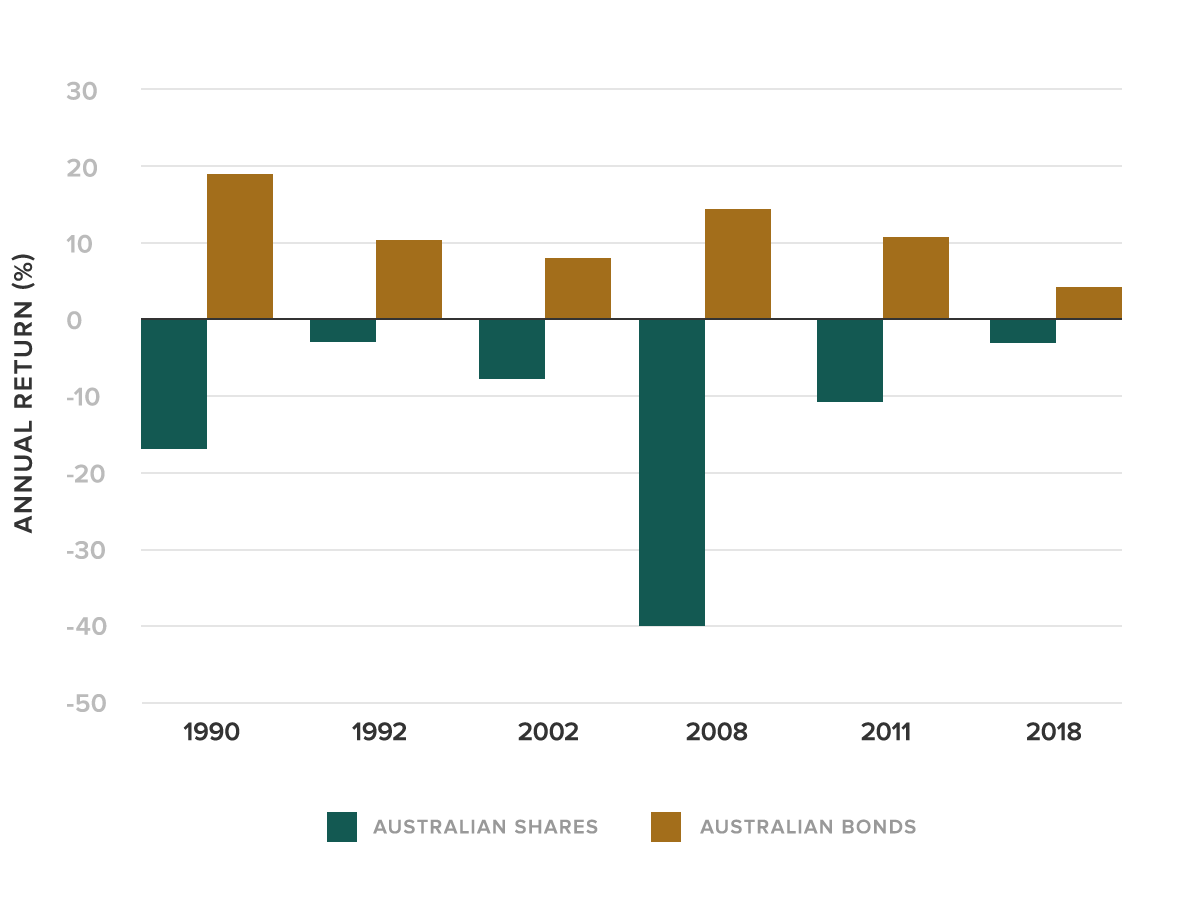

Cash is defensive because when markets fall it holds its value.

High grade bonds can do one better and rise when share markets fall. History backs this up too; in each of the 6 times Australian shares had a down year in the past 20, bonds rose to cushion the impact.

Can other assets be defensive?

This very much depends on the opinion of the fund manager and there is strong history to demonstrate why their opinions might not end up as fact.

High income stream and low growth assets

Just because an asset delivers a big income stream does not make it defensive. Take Telstra. Most of Telstra’s returns come from regular fully franked dividend income but its share price has dropped almost 50% since 2015.

Infrastructure and property assets

Much infrastructure and property is held in unlisted vehicles which raises three concerns:

- The value of the investment is the opinion of the fund manager and there is no way of knowing whether that value is credible given that there is no open market for the asset.

- The financial structure may see a return of capital reported as an income distribution.

- The investment is very illiquid and a sale is often extremely constrained by agreements with co-investors, including first right of refusal and so-called ‘tag-and-drag’ conditions. One critical characteristic of a defensive asset is to be able to sell it in a deep and open market.

The inherently risky nature of these investments is usually exposed towards the end of each market cycle when too much debt is loaded in to beef up returns.

In 2008 the Real Estate Investment Trust (REIT) sector fell by a whopping 75% globally because these funds had created income which couldn’t be sustained under high debts and falling prices.

During the Financial Crisis some super funds stopped members from transferring money out because they were unable to sell illiquid unlisted assets. One fund, MTAA super, lost $1.6 billion in 2011 due to poor hedging of unlisted assets. MTAA super lost its spot as one of the best performing funds in 2008 to become the second worst according to Super Ratings.

Creative definitions of defensive assets

In recent times many super funds have invented their own definition of a defensive asset which has helped to push them up the ratings.

Let’s look at this year’s top performing fund over the last five years according to Super Ratings, the Hostplus default balanced fund which claims a 24% allocation to defensive assets.

The Hostplus website explains that in addition to cash and fixed income “some asset classes, such as infrastructure, property and alternatives may have growth and defensive characteristics”.

Their self-defined defensive assets include infrastructure, credit, property and alternatives. These make up nearly all of the portfolio allocation to defensive assets. Government bonds and cash make up just 5% of the fund.

Hostplus Default Balanced Fund

| DEFENSIVE ASSET | PORTFOLIO ALLOCATION |

| Infrastructure | 12% |

| Property | 13% |

| Alternatives | 8% |

| Credit | 7% |

| Fixed Income | 0% |

| Cash | 5% |

| Total | 45% |

This has usually enabled Hostplus to regularly claim top gong in its chosen category. Hostplus isn’t the only one. Many of the top funds on this list have counted some other assets as defensive to make the Balanced fund weigh-in including Sunsuper, CareSuper, Mercy Super and Media Super.

Top 10 performing balanced funds over 5 years to 30 June 2020

| Rank | Fund Investment Option | Return |

| 1 | AustralianSuper – Balanced | 7.35% |

| 2 | UniSuper – Balanced | 7.28% |

| 3 | Cbus – Growth (Cbus MySuper) | 7.13% |

| 4 | Hostplus – Balanced | 7.01% |

| 5 | Mercy Super – MySuper Balanced | 6.82% |

| 6 | Vision SS – Balanced Growth | 6.75% |

| 7 | CareSuper – Balanced | 6.59% |

| 8 | First State Super – Growth | 6.56% |

| 9 | BUSSQ Premium Choice – Balanced Growth | 6.55% |

| 10 | Equip MyFuture – Balanced Growth | 6.54% |

Super funds can classify their own assets

Super funds aren’t required to disclose how they classify their investments – even to ASIC. They also aren’t required to share how each asset has performed or even what it is. This allows funds to play the ratings game without anyone holding them to account.

This can lead to problems, such as the large exposure Hostplus had with their unlisted assets Another big industry fund, REST Super, has also raised eyes for concern given the definition of their defensive assets.

Superannuation funds like Hostplus and REST are free to invest in illiquid unlisted infrastructure, alternatives and property assets. The issue is calling them defensive. This implies a lower level of risk, and is a problem for both the industry and the consumer.

How ratings agencies support tmis-leading self-reporting

Ratings agencies don’t properly query the allocations reported by the funds. This provides no check as to the real risk of the self-reported defensive assets.In addition, the ratings agencies have a few additional problems of integrity which we discussed in what fund ratings won’t tell you. To recap:

- Most ratings businesses only publicly announce the top performers and not the worst. This is because they are typically paid by the funds who they rate. Anyone who has seen The Big Short would understand how problematic this conflict of interest is.

It’s why we publish the Fat Cat Funds Report every year to shed a light on the best and worst funds.

Active or indexed super?

By our analysis, over 90% of active super funds underperformed an index fund of similar risk over five years after fees and taxes.

Expensive fees for active management is precisely what causes most super funds to underperform. For every active winner there has to be an active loser and management fees drag down net returns.

There are always going to be a small number of funds who beat the index but that group is always changing. Many funds in the top lists this year have also spent time near the bottom when markets weren’t as kind to them.

Let’s be clear, Hostplus and other Industry funds are making some good investments including into venture capital and infrastructure projects that will benefit Australia.

However what shouldn’t be making headlines and driving members to switch is how the fund performed compared to lower risk options in a rising market.

Remember, winners always change. Fees are with you every year. Make sure you compare your super fund with our Fat Cat Fund Report.

Chasing the latest returns harms investors

Over the last five years Hostplus has been one of the very few funds to almost generate enough extra returns to match an index fund of similar risk. Vanguard’s high growth fund still beat it after fees and taxes over one and three years.

Compared to the disastrous bank owned retail super products, industry funds consistently come out ahead. However that doesn’t mean some stakeholders aren’t massaging the truth about what drives returns and therefore what’s in the best interest of members.

Will Hostplus be able to keep up with an index fund over the next 10 years? Maybe, maybe not. Based on history, the odds of a fund that charges 1.45% per year beating a low cost index fund across the market cycle is not high.

Warren Buffett proved this when he recently won a 10 year bet that a Vanguard index fund would beat 5 expert-selected active fund managers.

Buffett backed the index fund which won by a massive 77%.