Exchange Traded Funds (ETFs) are among the most tax efficient methods of investing in Australia, so it is no surprise that they continue to grow in popularity.

The secret to their success is that ETFs have a lower turnover of shares and thus pay out fewer capital gains than managed funds and Listed Investment Companies (LICs), thus incurring less capital gains tax (CGT) come tax time.

Additionally, investors in ETFs typically inherit a lower tax bill during their holding period compared to other fund structures which need to distribute regular capital gains from redemptions or frequent rebalancing.

Whether you’ve invested in ETFs on your own, through a broker, or with the help of an online investing platform like Stockspot, we cover the following in this article:

- Why ETFs are tax efficient

- Lodging your tax return if you’re not a Stockspot client

- Lodging your tax return if you are a Stockspot client

This article will also take you through the following topics:

- Owning ETFs in your own name

- Australian share ETFs and franking credits

- Benefits of franking credits

- Capital gains on ETFs

- Capital loss tax

- Tax on ETF distributions

- Tax on foreign ETF income

- U.S. domiciled ETFs and the W8BEN Form

Why ETFs are tax efficient

ETFs have low portfolio turnover because they track an index and the investments within them aren’t bought and sold regularly. This means ETFs incur lower CGT compared to most active managed funds, which constantly trade and thus lead to higher CGT.

ETFs are also more tax efficient than managed funds because they trade on stock exchanges, such as the Australian Securities Exchange (ASX). Unlike unlisted managed funds, ETF portfolio managers do not need to sell the shares they’ve invested in to raise cash to pay investors who redeem or sell the fund.

For unlisted managed funds, this redemption process can lead to a CGT liability for all investors, regardless of how long they have owned the fund. If an ETF investor sells, it has no impact on other investors.

Lodging your ETF tax return if you aren’t a Stockspot client

If you invest in ETFs via another investment service, an overseas-based stock broker, a separately managed account or a managed investment scheme which uses a custody or trustee structure, tax can get complex.

It’s important to find out what tax information your provider will give to you at tax time each year, as it will differ from service to service and some won’t provide a comprehensive summary to help you prepare your tax.

If you own ETFs through another online broker you need to calculate your tax liability each year using the annual tax statements from each ETF you own.

To do this, combine the totals provided by each ETF as well as calculate any capital gains (or losses) that you’ve made during the financial year.

It’s also crucial to ask if you’re receiving the full benefits of:

- franking credits on your Australian ETF income

- the 15% withholding tax benefit on your overseas income

- the 50% capital gains discount on investments held for 12 months

Platforms and investment services which use an overseas custodian or a managed investment scheme structure may not be able to pass on all of these important tax benefits which can add up to 1% per year in extra returns.

Lodging your ETF tax return if you are a Stockspot client

If you’re a Stockspot client, we’ll combine the statements from all the ETFs you own with us.

This means if all of your ETFs are owned within Stockspot, you or your accountant will only need to use a single document to do your tax. Income from the individual ETFs and any capital gains will be summarised in your annual investor statement from us.

Find more about lodging your tax return with Stockspot.

ETFs tax: other considerations

Owning ETFs in your own name makes tax time easier

If you own ETFs through Stockspot, they will be owned legally and beneficially in your name on a Holder Identification Number (HIN) at the CHESS subregister.

If you don’t own your ETFs through Stockspot, you should check the ownership model of your broker.

From a tax perspective, direct ownership is the safest and most simple way to own ETFs, because it’s clear what income and capital gains you’ve made through the year.

Owning ETFs in your own name means you get full access to franking credits and don’t need to pay other people’s tax.

Australian share ETFs and franking credits

The dividend system in Australia can offer important advantages for investors in ETFs.

If Australian company taxes are already paid by the companies within an ETF, then investors don’t need to pay those taxes again at the personal level.

The corporate taxes paid are passed down to the Australian investor through tax credits (these are otherwise known as franking credits).

With ETFs, you receive the benefit of franking credits but are generally less reliant on them because your portfolio will be diversified across different sectors and asset classes.

For example, the Stockspot Model portfolios returned 0.25% to 0.64% in franking credit value in the 2023-4 tax period.

Benefits of franking credits

Franking credits can be used to reduce an investor’s total tax liability as they account for the taxes on dividends already paid by companies.

For individuals or complying superannuation entities, any excess franking credits can be refunded at the end of the year if the investor’s tax liability is less than the amount of the franking credits.

The dividends investors receive will only be taxed at their marginal tax rates. This is a big benefit for those on lower tax brackets including self managed superannuation funds (SMSFs).

Within the Stockspot Model Portfolios, for example, the Vanguard Australian Shares Index (VAS) distributes franking credits which we summarise for clients in their annual investors statement.

This makes it easy for you or your accountant to claim the full value of franking credits on your tax return. (If you have Stockspot Themes, you may have other ETFs that distribute franking credits.)

Capital gains on ETFs

ETFs tend to have lower capital gains tax liabilities than other investments, but if you sold any ETFs during the year, you will be required to calculate your CGT liability (if any) with respect to those ETFs.

ETF issuers won’t send a Capital Gains Tax Statement by default, so it’s up to you to calculate any capital gains and put it in the correct place on your tax return.

Where you’ve owned an ETF for more than 12 months, the taxation law allows the taxable capital gain to be reduced by 50% for individuals. This means that tax is only paid on half of the capital gain.

Capital loss tax

A capital loss (and capital loss tax) is when you deduct any allowable capital losses from a capital gain to reduce your capital gains tax.

This is different from an income tax loss. A capital loss can occur when you sell an asset for less than its taxable value against any capital gain for that same income year.

Capital losses can only be offset against any capital gains for that same income year. They might also be carried forward to offset future capital gains.

A capital loss on taxes cannot be offset against income.

This type of ETF tax strategy is used by investors to minimise their net capital gains during a particular financial year and are usually used at the end of a financial year.

The ATO has a great section on their website about using capital loss tax deduction in Australia to reduce capital gains.

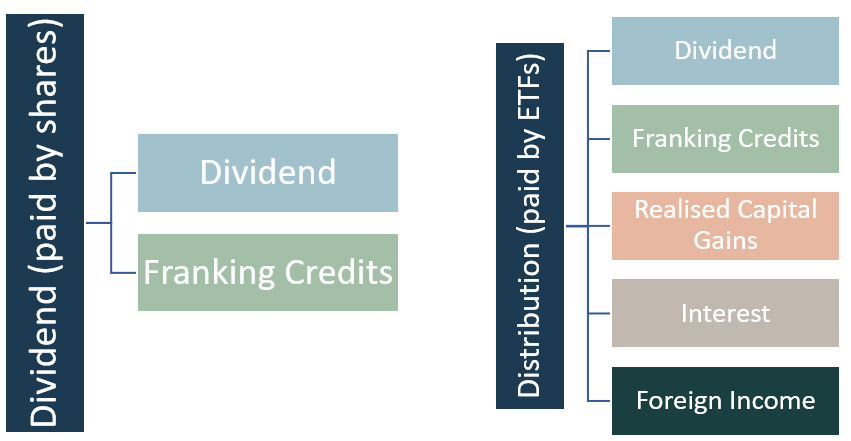

Tax on ETF distributions

A distribution from an ETF represents your share of the income earned by a fund. Each ETF may earn different types of income, such as dividends, realised capital gains or interest. Income may be Australian or foreign.

ETFs can be complex because they are structured as unit trusts, not ordinary shares. This means the types of income earned by an ETF can be split across different categories when they are distributed to you.

If you manage your own ETF portfolio, the income components required to complete your tax return will be shown in the annual tax statement posted to you or available to download from the registry website associated with each particular ETF.

In 2016, the ATO changed the rules around trusts by creating the Attribution Managed Investment Trust regime or AMIT. This has added further complexity to ETF tax.

If you’re a Stockspot client, we calculate the total distributions received from all the ETFs you owned during the year. It will be summarised in your Stockspot Annual Investor Statement. Find out more about lodging your tax return if you’re a Stockspot client.

Tax on foreign ETF income

Where an ETF invests in overseas companies, some of the income distribution may be withheld from investors. This is known as withholding tax.

The level of withholding tax varies depending on where the company resides and the tax rules in place between Australia and the residing country.

U.S. domiciled ETFs and the W8BEN Form

Australian investors who buy ETFs domiciled in the United States will incur a 30% withholding tax on any distributions. Australian investors are generally eligible to reclaim some of this back as a foreign tax credit, but will need to complete a W8BEN form to reclaim a 15% foreign tax credit.

In 2018 BlackRock converted 14 of their iShares US-domestic ETFs to Australian domiciled ETFs. This removed the W8BEN form for investors in the following ETFs: IAA, IEM, IEU, IJH, IJP, IJR, IKO, IOO, IRU, ITW, IVE, IVV, IXI, IXJ and IZZ.

There are no ETFs within the Stockspot core portfolios (Model or Sustainable) that require investors to complete a W-8BEN form to claim back tax. (If you have Stockspot Themes, this may not be the case).

We hope this article has helped you figure out some of the tax implications of ETFs. As always, if you have any questions or comments, we’d love to hear from you.

Disclaimer: This article is general information only and doesn’t consider any individual’s personal circumstances. ETFs offer a range of tax advantages for Australian investors, however everyone’s individual circumstances are different. Each ETF can also have a different tax treatment.

You should consult with your accountant to learn more about the tax consequences of owning ETFs and how it may impact your overall tax. This is particularly important if you are a non tax resident of Australia or are investing via a trust, company or Self Managed Super Fund.

The Australian Taxation Office (ATO) also has a helpline for personal tax enquiries, which is 13 28 61. In addition, the ATO has a number of publications which will help you understand what you need to do to complete your return.

Updated 17 June 2024. Previously updated 7 June 2022. First published June 2021.