Investors are familiar with receiving dividends from shares they own. However, when it comes to ETFs, the income received is known as a distribution. While these terms are often used interchangeably, they actually refer to different concepts, which can lead to confusion. This article will clarify the differences between a dividend and a distribution, helping you better understand how each works

- What is a dividend?

- What is a distribution?

- Dividend yield vs distribution yield

- Tax on distributions

What is a dividend?

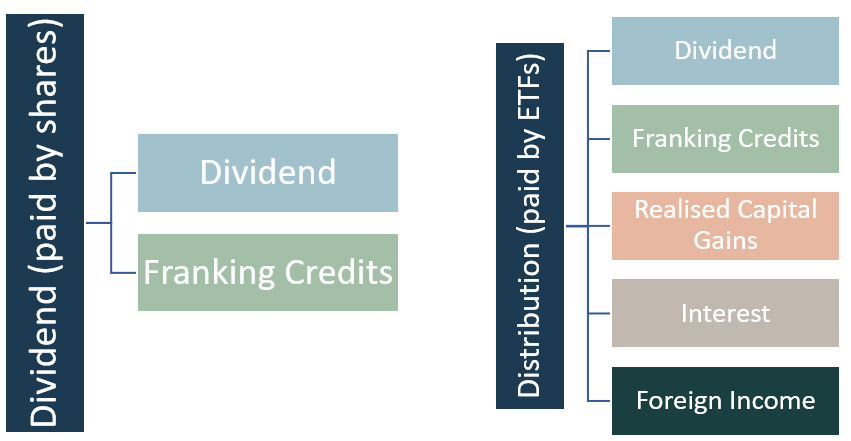

When you buy a share on the ASX, you become a part-owner of that company. Your returns can come from two main sources: growth in the share price (known as capital return) and cash payments from the company’s profits (known as dividends or income return).

When a company earns a profit, it has options: it can reinvest the money to fuel further growth, distribute it to shareholders as dividends, or do a combination of both. Companies that pay dividends typically do so at regular intervals, such as quarterly or half-yearly.

Australia is home to some of the world’s highest dividend-paying companies, including big names like the major banks, BHP, and Telstra. These companies are particularly appealing to Australians seeking income, especially in a low-interest-rate environment.

What is a distribution?

When you invest in an ETF such as the Vanguard Australian Shares Index ETF (ASX: VAS), you benefit from all of the companies within that ETF that pay dividends.

A distribution is your share of the income generated by the investments held in the fund. The ETF collects all forms of income and profits made by the fund and then distributes it to the unit holders (that’s you, the investor) as distributions.

Instead of receiving individual dividends from each company (which would be highly complex to manage), you receive a distribution from the ETF. This distribution includes all the dividends paid by the companies within the ETF during the most recent period, along with any other income sources. It’s a much simpler way to receive dividends. Even better, if you invest with a service like Stockspot, we combine all of your distributions into a single, easy-to-understand tax summary document.

A key benefit of investing in an ETF over a LIC (listed investment company) is that all income must be distributed as we discuss in our analysis of ETFs v LICs. An ETF collects dividends and other forms of income on behalf of investors and pays it to them at scheduled intervals. For example, the Vanguard Australian Shares Index ETF pays out its distributions quarterly (January, April, July and October).

A typical ETF distribution can be broken down into five main components:

- Dividends – ETF receives dividends from the companies it owns and will pass on each investors portion and associated franking credits.

- Franking credits – ETFs are eligible to pass on franking credits which we discussed here.

- Interest – like bond ETFs receive interest (i.e. coupon payments) from the underlying bonds they own.

- Realised Capital Gains – from buying and selling the underlying shares (e.g. incurred during rebalancing) with any net capital gain passing on to the investor.

- Foreign income (e.g. ETFs that own overseas shares) and any associated foreign tax credits.

Dividend yield vs distribution yield

When you buy a share, you can calculate its historic dividend yield by taking the total dividends paid over the past 12 months as a percentage of the current share price. For example, if a company paid $0.40 in dividends over the last year and its share price is $10, the dividend yield would be 4%.

Similarly, when you own an ETF or another unit trust, you can calculate the distribution yield by taking the total distributions paid over the past 12 months as a percentage of the ETF’s current price. For instance, the Vanguard Australian Shares Index ETF (ASX: VAS) has paid $3.43 in distributions over the last year, and with a unit price of $84.10, it has a distribution yield of 4%.

In both cases, you can choose to calculate the dividend or distribution yield either including or excluding franking credits.

Tax on distributions

Similar to dividends, distributions from ETFs form part of your assessable income from a tax perspective.

If an ETF owns shares in Australian tax paying companies it may receive franked dividends. Franking credits are paid to the ETF which then get passed to the end investor as part of the ETF distribution. The ETF provider will show the amount of franking attached to its distribution.

ETFs can make tax quite confusing by issuing a long document at the end of the financial year called an attribution managed investment trusts (AMIT) annual tax statements. This statement will show all the components of the ETF distributions over the financial year.

We’ve built technology to make tax time simple when you own ETFs with Stockspot. We calculate the total distributions received from all the ETFs you owned during the year and summarise it in your one-page annual investor statement.

You can find out more about how ETFs are taxed in our explainer article. Stockspot doesn’t provide tax advice and we encourage investors to seek advice from an accountant or qualified tax professional.