The 2026 Federal Budget introduced some of the biggest investment tax changes Australia has seen in decades.

The changes to capital gains tax, trust distributions and negative gearing will affect many Australians building wealth through ETFs, shares, investment property and small businesses.

Importantly though, while the changes have now been announced, they still need to pass through the full legislative process before becoming law. The final details may still evolve over time as Treasury releases draft legislation and consultation begins.

Like all tax policy, there’s also the possibility that future governments may amend or reverse some of these changes over time. Australia’s tax system has changed many times over recent decades and will likely continue evolving in the future.

For investors, that’s an important reminder not to panic or make rushed decisions based purely on headlines. Diversification, long term thinking and tax efficient investing still matter enormously.

In this article, we explain what changed in the Budget, what it could mean for investors and some of the practical implications for Stockspot clients.

What changed in the 2026 Federal Budget?

The biggest reform announced was the replacement of the current 50% capital gains tax discount with a new inflation indexation system combined with a minimum effective 30% tax floor on many capital gains.

Under the previous system, Australians who held an investment for more than 12 months generally only paid tax on half of the capital gain.

Under the new rules, investors will instead increase the original purchase price of the asset by inflation before calculating the taxable gain.

In periods of relatively low inflation, this will generally result in materially more tax being paid than under the previous 50% discount system. Treasury argues the previous fixed 50% discount often overcompensated some assets for inflation, particularly detached housing, while undercompensating others during certain periods.

For assets held before 1 July 2027 and sold afterwards, the Government says gains accrued before and after commencement will effectively be treated under different tax systems. Capital gains accrued before 1 July 2027 may continue to partially access the previous 50% CGT discount, while gains accruing afterwards will fall under the new indexed regime and minimum tax framework.

The Government says taxpayers will be able to either obtain a formal valuation at 1 July 2027 or use an ATO apportionment formula to estimate the split between the two periods.

The Budget also introduced:

• a minimum 30% tax rate on many discretionary trust distributions

• restrictions limiting negative gearing concessions to newly built residential property

• broader reforms intended to increase taxation of long term capital gains and investment income.

The Government says existing negatively geared properties will largely be grandfathered under the current rules. However, purchases of existing residential investment properties made after 7:30pm on Budget night are expected to lose access to full negative gearing benefits under the new framework.

The Government also announced that assets acquired before the original introduction of CGT in 1985 may become partially subject to CGT, with gains accruing after 1 July 2027 expected to fall under the new indexed regime.

Combined together, these changes represent one of the largest shifts in Australia’s investment taxation system in decades.

Why this matters for investors

For long term investors, the biggest issue isn’t just the higher tax rate itself. It’s the impact on long term compounding. Even relatively small increases in tax drag compound significantly over time.

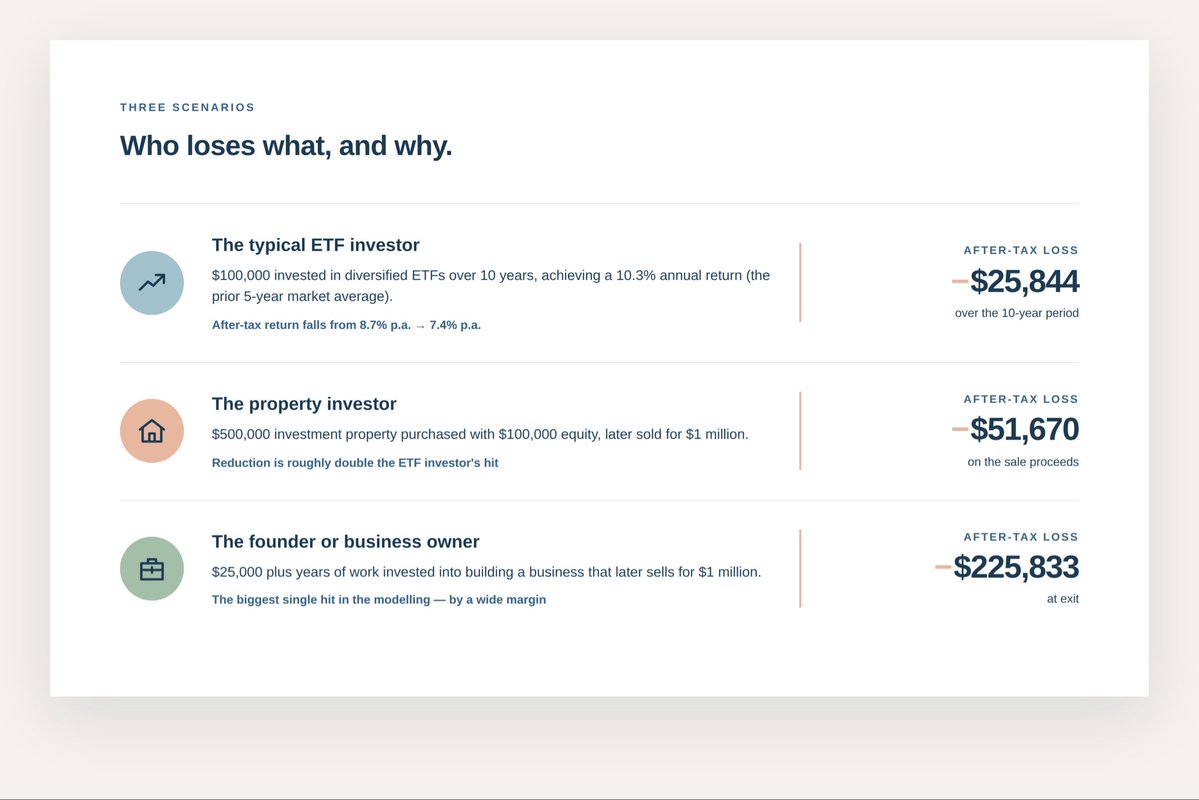

To help Australians understand the impact, we’ve built a new CGT calculator that estimates how the changes could affect different investment scenarios over time.

The projected differences can become substantial over long periods.

An ETF investor growing $100k over 10 years could end up with around $26k less after tax. A property investor could lose more than $50k in after tax wealth. A founder building and selling a business for $1m could lose more than $225k.

For younger Australians still building wealth, those differences matter enormously.

The changes effectively increase the amount many Australians will need to save and invest to reach the same long term financial goals.

Over time, the changes may also alter how capital flows across the economy. When governments change tax settings, investors naturally gravitate toward more tax efficient structures and assets.

That means investments driven primarily by long term capital growth may become relatively less attractive, while assets generating ongoing income or benefiting from concessional tax treatment may become relatively more attractive.

Which investments may become less attractive?

Investment property

Investment property becomes materially less attractive under the new rules.

The combined impact of higher capital gains tax and removed negative gearing benefits changes the economics of leveraged property investing significantly, particularly for investors relying heavily on long term capital appreciation.

Based on the Budget papers and subsequent Treasury commentary, existing negatively geared properties are expected to be grandfathered under the current rules. However, future purchases of existing residential property lose access to negative gearing benefits.

Over time, this may reduce speculative demand for existing residential property but reduce the stock of rentals.

Active managed funds and unit trusts

High turnover active funds and unit trusts may also become less attractive.

When portfolio managers buy and sell investments within a trust structure, realised capital gains are generally distributed directly to investors each year regardless of whether the investor personally sold anything.

Under higher CGT settings, that ongoing tax drag becomes much more painful.

Funds with high turnover strategies could generate significantly larger annual tax liabilities for investors compared to lower turnover investment approaches.

Startups and small companies

The changes may also disproportionately impact startups, venture investing and smaller growing companies.

These investments already involve substantial downside risk and long holding periods. If the eventual upside becomes taxed more heavily, the risk reward equation changes materially.

Over time, that may reduce incentives for entrepreneurship, venture capital formation and investment in smaller growing businesses.

Australia already competes globally for capital, talent and innovation. Tax settings play an important role in where founders choose to build businesses and where investors choose to allocate long term capital.

I wrote more about the potential impact on entrepreneurship and innovation in a recent article for The Australian.

Gold and cryptocurrency

Assets like gold and Bitcoin may also become relatively less attractive because most of their return typically comes through capital appreciation rather than ongoing income generation.

When gains become more heavily taxed, investors may increasingly avoid realising gains altogether or look for alternative financing structures like margin loans that avoid triggering taxable events.

Which investments may become relatively more attractive?

Passive ETF investing

Passive ETF investing may become even more attractive relative to active management and high turnover trading strategies.

ETFs generally realise fewer capital gains over time, resulting in lower ongoing tax drag and fewer taxable events.

This is one reason many Stockspot clients already benefit from long term diversified ETF investing compared to higher turnover active strategies.

The new rules may widen this after tax advantage further.

Blue chip dividend shares

Large dividend paying companies may also become relatively more attractive.

Companies like BHP, Telstra and Commonwealth Bank generate a larger proportion of investor returns through dividend income rather than long term capital growth.

If capital gains become more heavily taxed, investors may place greater value on reliable income streams and franking credits.

Superannuation

Superannuation may become significantly more attractive relative to investing outside super.

Because super already operates under concessional tax settings, many investors may increasingly prioritise concessional and non concessional contributions over time.

Ironically, this may also mean older Australians with larger super balances are relatively less impacted than younger Australians still building wealth outside super.

However, the trade off remains that super capital is largely locked away until preservation age and contribution caps still limit how much investors can move into the system.

Bonds and defensive assets

Government bonds and defensive income assets may also become relatively more attractive because most of their returns already come through income rather than capital appreciation.

How the new tax changes may affect different investments

| Investment / structure | Likely impact from the new tax changes | Why |

| Investment property | Less attractive | Higher CGT combined with removed negative gearing benefits changes the economics of leveraged investment property investing |

| High turnover active funds and unit trusts | Less attractive | Frequent buying and selling creates ongoing realised capital gains that are generally distributed directly to investors each year |

| Startups and small business investing | Less attractive | Higher tax on eventual upside may reduce incentives for entrepreneurial risk taking |

| Gold and cryptocurrency | Less attractive | Returns rely heavily on capital growth rather than ongoing income |

| Passive ETFs | Relatively more attractive | Lower turnover generally means fewer realised gains and better tax deferral |

| Blue chip dividend shares | Relatively more attractive | A larger share of returns comes from dividend income and franking credits |

| Superannuation | More attractive | Super retains concessional tax treatment relative to investing outside super |

| Primary residence | More attractive | The family home remains largely exempt from capital gains tax, increasing its relative tax advantage |

| Bonds, defensive income assets and term deposits | More attractive | A larger proportion of returns already comes through income rather than capital growth |

What Stockspot clients should focus on

The most important thing is not to panic or make rushed investment decisions.

Tax matters, but good investment behaviour still matters more.

For most investors, the key principles remain the same:

- stay diversified

- focus on long term goals

- minimise unnecessary turnover

- avoid emotional reactions to headlines

- prioritise tax efficiency where possible.

Stockspot portfolios are already designed around many of the principles likely to become even more valuable under the new rules, including:

- low turnover ETF investing

- diversified long term asset allocation

- automated tax reporting

- optional “buy only” rebalancing.

The new time weighted CGT system is also likely to create major administrative complexity for investors manually managing portfolios across multiple brokers and CGT tax structures.

Stockspot expects to update its tax engine and reporting systems to reflect the final legislation once implementation details are confirmed. That means clients shouldn’t need to manually calculate split tax treatments themselves.

The broader economic impact

The Government argues these reforms could improve long term productivity by reducing distortions that favour leveraged property investment and encouraging capital to flow toward more productive parts of the economy.

Supporters of the reforms argue Australia’s existing tax system excessively favoured leveraged investment in existing housing over productive business investment, while also contributing to housing affordability pressures and intergenerational inequality.

There is some merit to that argument. Australia’s tax system has long provided strong incentives for leveraged property investment, particularly into existing housing stock rather than new productive capacity.

However, the broader economic question is whether the reforms genuinely redirect capital toward productive investment, or whether they simply reduce the after tax reward for long term risk taking more broadly.

The challenge is that the package doesn’t just reduce incentives for leveraged property investment. It also materially reduces after tax returns for long term equity investing, startup formation, venture capital and entrepreneurial risk taking more generally.

If the tax burden on long term capital formation rises across the board, capital doesn’t automatically flow into more productive investments. In many cases it may simply become more defensive, more short term or increasingly flow offshore toward jurisdictions with lower effective tax rates on investment and entrepreneurship.

The irony is that Australia already struggles with weak productivity growth, slowing business dynamism and an economy already heavily concentrated around large incumbent companies. Reducing the long term after tax upside from building companies or investing in growth assets risks reinforcing those trends rather than improving them.

There’s also a broader policy contradiction in simultaneously arguing that Australia needs more innovation, more venture capital and more entrepreneurial risk taking while materially increasing the tax burden on the eventual upside that makes those risks worthwhile in the first place.

The biggest consequence of major tax changes isn’t just the tax itself. It’s how behaviour changes across the economy. If long term risk taking becomes less rewarding, capital naturally shifts toward safer and more tax efficient assets.

Over time, that may reduce the flow of capital into startups, productive businesses and long term growth projects. At the same time, more capital may increasingly flow toward superannuation, owner occupied housing and lower risk income generating investments.

There may also be broader inflationary implications over time. If long term investing and capital formation become materially less attractive after tax, some households may choose to consume more today rather than defer consumption into long term investment assets. Reduced incentives to save and invest can potentially increase short term consumption across the economy, which may place additional upward pressure on inflation and interest rates over time.

There are also questions around whether the Government’s projected tax revenue will ultimately materialise in full.

Higher capital gains taxes can also create stronger “lock in” effects, where investors delay selling assets to defer tax liabilities. Over time, that can reduce capital mobility and discourage portfolio reallocation even when capital could potentially be deployed more productively elsewhere.

When capital gains taxes rise materially, investors adapt. Some may hold assets for longer. Others may restructure investments to reduce taxable events altogether.

As a result, realised gains and taxable activity may ultimately fall over time.

Final thoughts

Tax rules will change over time, but the core drivers of long term wealth creation remain remarkably consistent.

Diversification, discipline and compounding still matter. And tax efficient investing is likely to become even more important going forward.

Over the coming months we’ll continue publishing updated analysis, and practical guidance to help Stockspot clients understand the changes and stay focused on their long term financial goals.