The last few weeks have been a stomach-churning ride for some investors. The impact of the Coronavirus pandemic, a growing number of job losses and a looming recession continue to take their toll on global share markets.

It may seem like a sensible decision to exit markets and move to cash after seeing the Australian share market fall by 34% in a matter of months. At least until things settle down.

However, is moving to cash in your best interest and what are the risks of this strategy?

We’ve recently discussed:

What coronavirus means for your portfolio and

Why we’re rebalancing portfolios now.

In this article we’ll cover:

- The risk of short term market timing

- Why moving to cash costs more than you think

- The impact of tax and transaction costs

The risk of short term market timing

For even the most seasoned of investors, watching the value of your investments decline is never easy.

When share markets fall sharply, emotions can take over and feelings of fear, panic and discomfort can set in. Minimising further losses and moving to cash can seem like the best, most logical thing to do. Even if that means abandoning your investment plan which had carefully considered your long term goals, comfort with risk and time horizon.

It’s important to think about the consequences and how this may impact your future.

The decision of when to get out is the easy part.

But then what? What’s your plan once it’s in cash earning little to no interest? This is where things get more tricky.

The re-entry strategy is the often overlooked part of this decision process, and if you get the timing wrong it comes at a sizeable cost. It could mean you miss out on years of returns.

Just days after the Australian share market reached a seven year low on 23 March 2020, it bounced back by 16% over three consecutive days. The steepest climb since 1931. Then on March 30 we saw the single largest up day in the Australian share market in decades.

This might seem unusual, but in fact, it’s not.

Large down moves in the share market are followed by big up days. Moving to cash means you miss out on the market bounce. If you miss out on two days when the market rises 5% because you’re in cash, that could be a whole year worth of returns you’ve foregone.

Why moving to cash costs more than you think

It’s fair to say, moving to cash will offer some level of comfort in the short term, knowing your money is in a bank account where it won’t decrease in value any further (or so you think).

But what about long term? What is the impact based on when you start investing again?

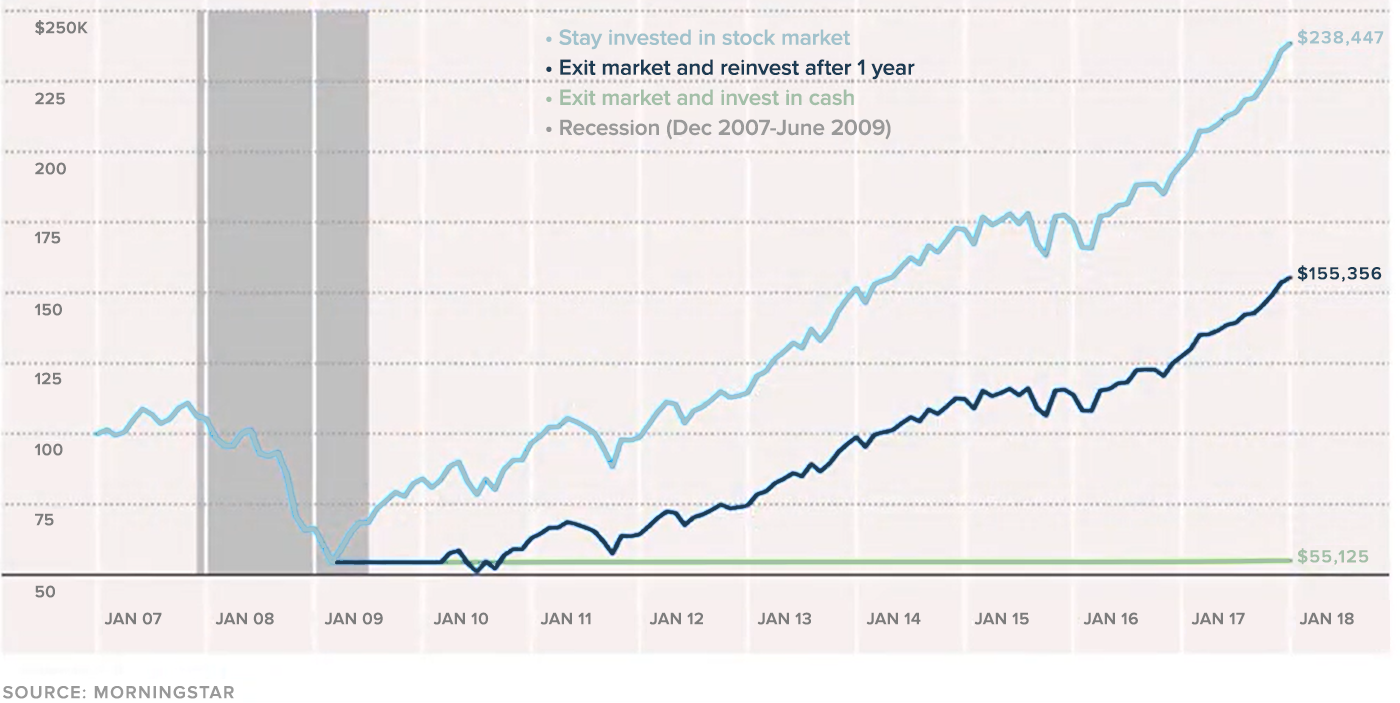

The chart below compares different investing strategies during the Global Financial Crisis (GFC) of 2007-2009.

It shows the growth of a $100,000 portfolio invested in over the next ten years based on three different choices you could have taken.

1) Stay invested in the share market through the GFC and the following 10 years

2) Exit the share market in January 2009 (when the portfolio had fallen to approximately $50,000), and then re-enter one year later

3) Exit the share market in January 2009 (when the portfolio had fallen to approximately $50,000), and stay in cash for the next 10 years

The differences in end results are staggering.

An investor who moved to cash during the crisis and stayed there for the next 10 years (green line), would have seen their $50,000 portfolio grow to just $55,125.

If you waited it out a year for markets to settle down you would have ended with $155,356.

Meanwhile an investor who did absolutely nothing and rode out the market volatility would have ended with $238,447, a return of 375%.

The results were similar after the 1987 crash, showing that moving to cash after a large market correction can be an expensive mistake over the following years.

The impact of tax and transaction costs

There’s another reason you might want to reconsider moving to cash – tax.

From a tax perspective selling your investments can lead to realising capital gains in the short term. Any money you pay in tax now is money that isn’t invested and compounding for you.

A whitepaper by BOS Invest shows investors who move in and out of the market lose an additional 0.6% p.a. in returns due to tax and transaction costs.

This table shows the impact of staying in cash over different periods of time during the year.

| Percent of time period invested in cash | Loss in Annual Return before tax and transaction costs | Loss in Annual Return after tax and transaction costs |

| 5% | 0.23% | 0.83% |

| 10% | 0.46% | 1.06% |

| 15% | 0.69% | 1.29% |

| 20% | 0.93% | 1.53% |

| 25% | 1.11% | 1.71% |

| 30% | 1.31% | 1.91% |

| 35% | 1.54% | 2.14% |

Source: BOS Invest

Key takeaways

While it might make you more comfortable in the short term, moving to cash can be an expensive move over the long term. Markets do recover so moving to cash for an extended period is unlikely to put you in a better position, especially in a low interest rate environment.

It’s still important to review your investment profile periodically to ensure you’re taking the right amount of risk. But once that’s done, try and stay on top of your emotions, ride out the ups and downs in the market and stay focused on your long term goals.

The Stockspot Goal Tracker is one way of doing just that.