A couple of weeks ago I wrote about a major flaw in the government’s proposed capital gains tax reforms.

Using a simple four share portfolio, I showed how replacing the current 50% capital gains tax discount with inflation indexation could increase the amount of tax paid by investors by 61%.

The example was deliberately simple because it helped illustrate the mechanics of the problem. But some readers reasonably questioned whether a portfolio containing one extreme winner, two mediocre performers and one complete failure was representative of how Australians actually invest in shares.

A subsequent article in the AFR recently challenged the view that the proposed CGT changes would make direct share investing less attractive, using a simple portfolio of three Australian bank shares to show that the tax outcome would be broadly unchanged.

While it’s a useful illustration, the difficulty with that analysis is that it suffers from a form of survivorship and selection bias. Real investors don’t have the benefit of hindsight when choosing investments. Most share portfolios contain a mix of exceptional winners, disappointing losers and investments that simply tread water. A portfolio made up entirely of three large bank shares is unlikely to reflect how most Australians actually build wealth over time.

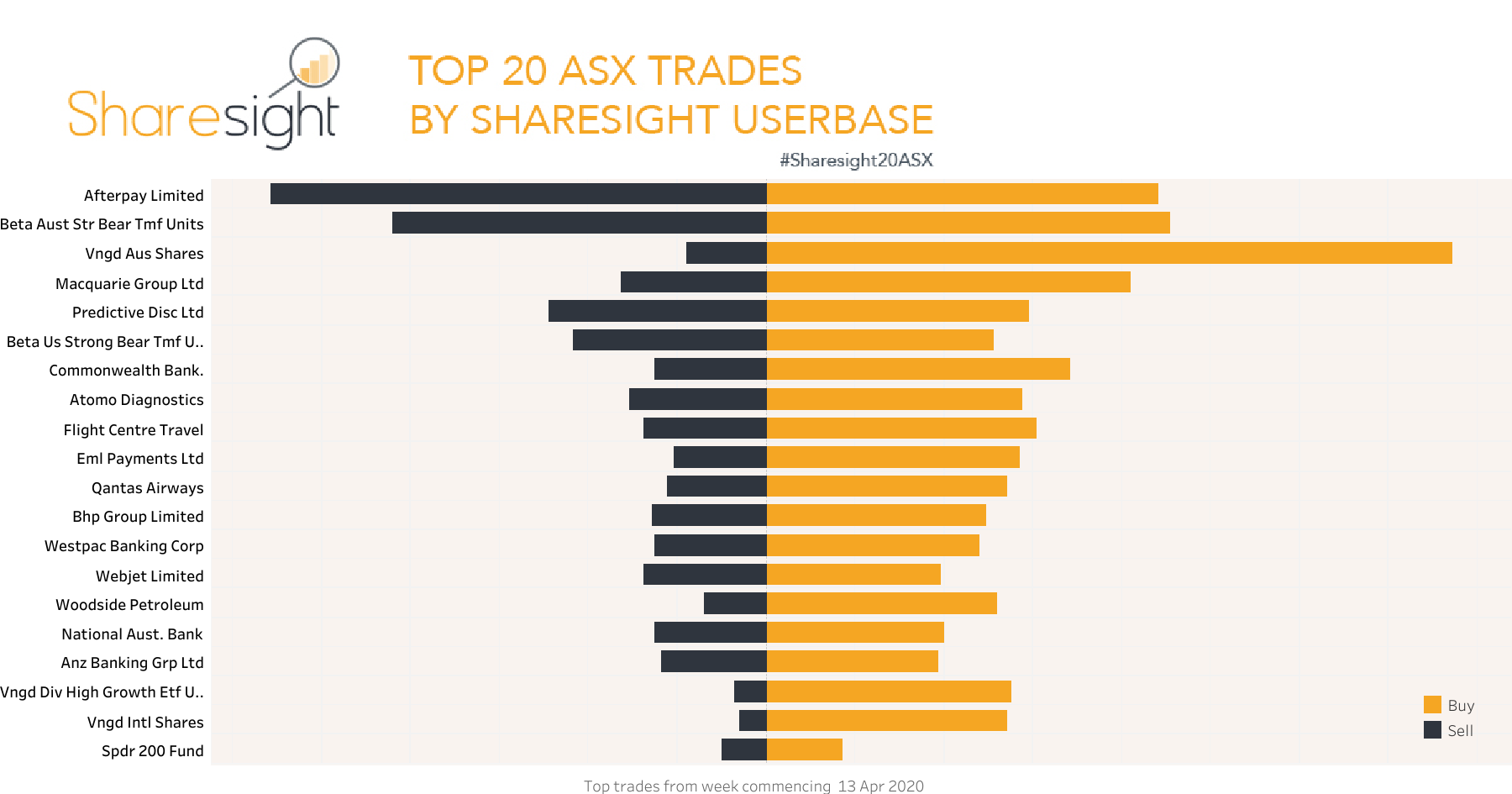

So I decided to test the reforms using a portfolio based on actual investor behaviour rather than relying on a hypothetical portfolio. I analysed the 20 most popular ASX shares and ETFs purchased by Sharesight users during April 2020 which I found on their blog. Importantly, these were not random investments. They were the shares Australians were actively buying during the COVID lockdowns, one of the most significant periods of investing activity in modern history, making them a useful proxy for how retail investors actually build wealth over time.

Unlike a portfolio of three major banks, the Sharesight portfolio contained exceptional winners, mediocre performers and outright failures. In other words, it looked much more like the portfolios real investors actually own.

The results were remarkably similar to our original example.

Despite analysing a completely different portfolio based on actual investor behaviour, I arrived at a very similar conclusion as the original hypothetical example. The proposed indexation model increased taxable gains by approximately 82%.

The reason is slightly different in this case. In the original example, much of the tax increase came from the inability to fully recognise real losses. In the Sharesight portfolio, the larger impact comes from the concentration of capital returns in a handful of exceptional winners, whose gains become far more taxable under the proposed framework.

That suggests the issue is not a quirk of a hypothetical example or a particular portfolio construction. It appears to be a structural flaw of the proposed system, one that emerges whenever a diversified portfolio contains a small number of large winners alongside a mix of average and unsuccessful investments.

The portfolio

The portfolio consists of the 20 most popular ASX securities traded by Sharesight investors in April 2020, with $10,000 invested into each holding.

The list included several of Australia’s strongest performing investments over the period, including Afterpay, BHP, Macquarie Group, Commonwealth Bank as well as some successful ETFs like VAS and VGS. It also included a number of mediocre performers and a handful of outright losers.

What happened to the portfolio?

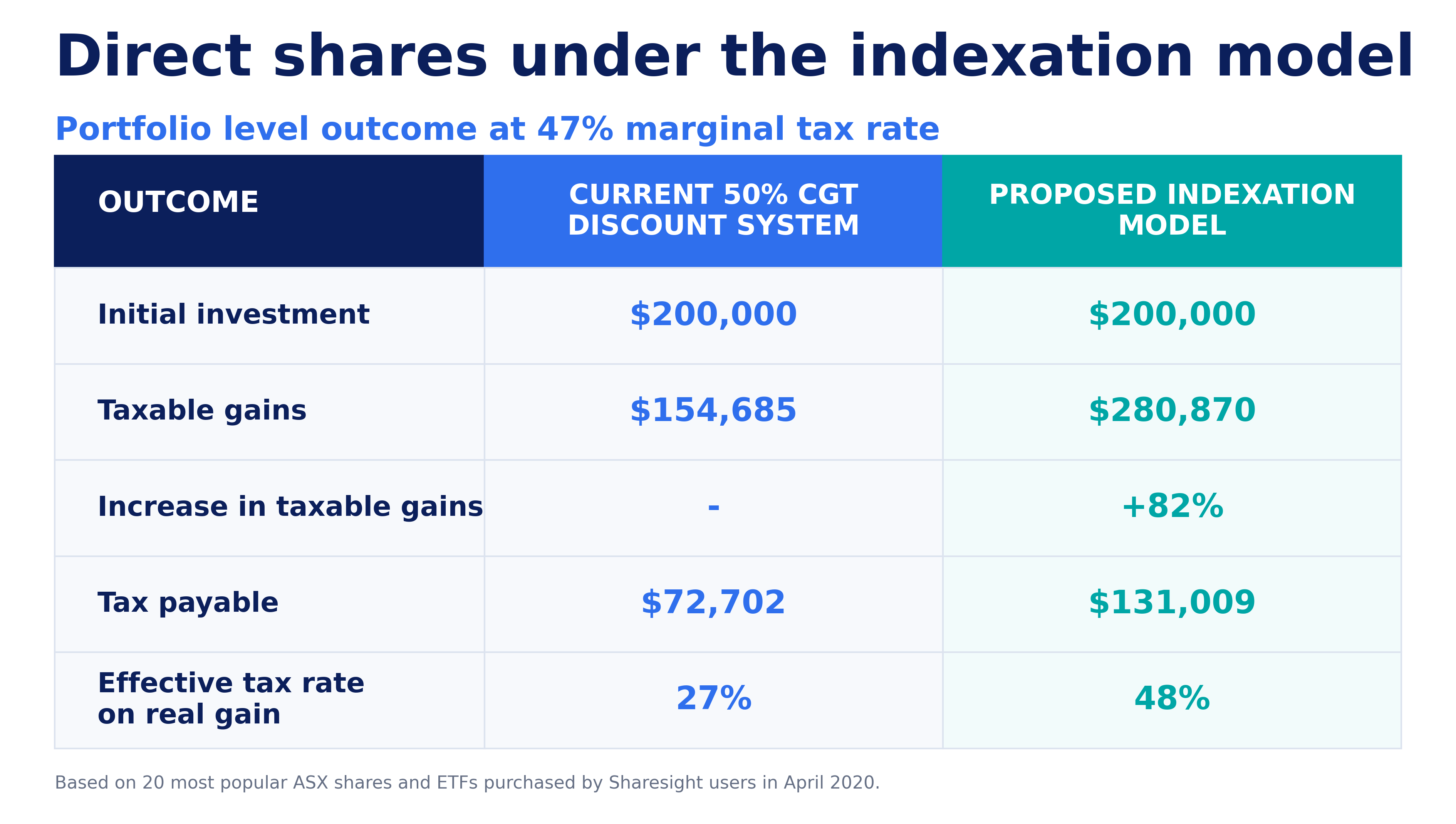

Over the six year period from April 2020 to June 2026, the $200,000 portfolio generated nominal gains of $309,370. After adjusting for inflation, the investor’s true economic gain falls to $271,370, representing the actual increase in their purchasing power. Under the current system, the taxable gain is $154,685 after applying capital losses and the 50% CGT discount. Under the proposed framework, gains are indexed but real losses are not fully recognised. As a result, the taxable gain rises to $280,870, which is higher than the investor’s total real economic gain and 82% higher than under the current system.

The winners get bigger

The proposed system significantly increases the taxable gain generated by the portfolio’s biggest winners. The table below shows several of the strongest performing investments.

| Investment | Nominal Gain | Taxable Gain Under Current 50% Discount | Taxable Gain Under Proposed Indexation | Increase |

| Macquarie Group | $20,682 | $10,341 | $18,782 | +82% |

| Commonwealth Bank | $24,115 | $12,058 | $22,215 | +84% |

| Vanguard International Shares ETF | $14,262 | $7,131 | $12,362 | +73% |

| Afterpay | $18,624 | $9,312 | $16,724 | +80% |

| BHP Group | $24,682 | $12,341 | $22,782 | +85% |

Under the current system, investors receive the benefit of the 50% CGT discount on long term gains. Under the proposed system, those gains become largely taxable in full once adjusted for inflation. For the portfolio’s strongest performers, the taxable gain increases by 73% to 85%.

The weaker investments provide less protection

While several holdings delivered exceptional returns, others failed to beat inflation or produced outright losses. Under the current system. those gains and losses broadly offset each other across the portfolio before the 50% CGT discount is applied.

Under the proposed indexation model, failed investments in a direct share portfolio only generate nominal capital losses even though their real economic loss after inflation is larger.

| Investment | Real Economic Loss | Recognised Capital Loss Under Proposed System | Unrecognised Real Loss |

| BBUS | $11,221 | $9,321 | $1,900 |

| BBOZ | $10,079 | $8,179 | $1,900 |

| Atomo Diagnostics | $11,450 | $9,550 | $1,900 |

| EML Payments | $10,241 | $8,341 | $1,900 |

| Webjet | $2,220 | $320 | $1,900 |

In this example, 15 of the 20 investments generated returns above inflation and only 5 produced losses. In other words, it was a relatively successful portfolio.

Many real world portfolios don’t look like this. Over longer time periods, or in sectors such as mining exploration, biotechnology and venture capital, a small number of exceptional winners often generate most of the returns while many other investments deliver mediocre results or lose money.

When that happens, the gap between an investor’s actual economic gain and their taxable gain becomes larger still. That’s what occurred in the original four share example, where the effective tax rate on the investor’s real gain rose to around 70%.

The portfolio level outcome

The most important comparison is at the overall portfolio level. The portfolio generated a real economic gain after inflation of approximately $271,000. Yet the taxable gain differs dramatically depending on which tax system is applied.

The investor earned exactly the same return, the portfolio is identical and the inflation adjusted gain is identical. The only difference is the way the gain is measured for tax purposes. The tax bill rises by approximately 82% or $58,000.

Why Treasury’s modelling underestimates the impact

The government’s public Budget modelling works reasonably well when applied to broad market index ETF returning 4-5% p.a. because an index ETF behaves like a single compounding investment.

This is one reason why I recently explained on Livewire that diversified index ETFs may be among the biggest beneficiaries of the Budget, as their structure naturally mitigates many of the distortions created by the proposed tax changes.

But many Australians don’t invest exclusively through broad market ETFs.

Millions of Australians hold portfolios of direct shares, small companies, emerging businesses, technology stocks, thematic ETFs or startups. These portfolios naturally contain a much wider dispersion of returns between winners and losers.

Ironically, the more diversified your share portfolio becomes, the more likely you are to encounter this issue because diversification naturally increases the spread between exceptional winners and disappointing investments.

That’s why the Sharesight data is so revealing. Sharesight is widely used by self directed investors who typically hold diversified portfolios of individual shares and ETFs. If there is a group likely to be affected by the interaction between extreme winners and weaker performers, it’s this one.

The source of the tax increase varies depending on the type of portfolio, but the direction of the impact is remarkably consistent.

In high growth portfolios, the increase is driven primarily by the more punitive treatment of large capital gains. A small number of exceptional winners generate most of the wealth, and those gains become far more taxable under the proposed framework.

In lower return portfolios with a wider spread of winners and losers, the problem shifts. The inability to fully recognise inflation-adjusted losses means investors can end up paying tax on gains that substantially exceed their true economic profit. While the increase in taxable gains may be smaller in dollar terms, the proportion of the investor’s real return lost to tax can be even higher despite the portfolio generating less wealth overall.

Put simply, investors are penalised whether their portfolio performs exceptionally well or only moderately well. The mechanism changes, but the outcome remains the same. Strong portfolios are penalised because their winners become more taxable. Weaker portfolios are penalised because their losses become less deductible.

A real world confirmation

The most important takeaway from this analysis isn’t the exact tax rate. It’s how closely the result mirrors our earlier hypothetical example.

In the original example, the proposed framework increased taxable gains by 61%, from $43,500 to $70,000. In this real world portfolio, based on the actual investment choices of thousands of Australian investors, taxable gains increased by 82%, from $154,685 to $280,870.

The numbers differ, but the underlying result is remarkably similar.

Policymakers should carefully consider whether a tax system that increases taxable gains for a typical long term investor by more than 80% is really achieving its intended objective.

The government’s stated aim is to improve fairness and encourage investment into housing. Yet if the practical effect is to penalise diversified share investors and significantly increase tax on ordinary Australians who build wealth patiently over decades, the reforms risk creating distortions far greater than those they seek to address.

Over the past 30 years, Australia successfully encouraged millions of people to become investors, shareholders and business owners. The tax system broadly rewarded patience, risk taking and long term ownership.

A danger of these reforms is that they undermine those incentives by substantially increasing the tax burden on exactly the investors who do what policymakers have long encouraged them to do: save regularly, diversify broadly and invest for the long term. As I recently wrote in The Australian, over the past 30 years Australia taught millions of ordinary people how to become investors. These reforms risk teaching the next generation not to bother.