In my recent opinion piece published in The Australian, I argued that supporters of capital gains tax reform are right about one important thing.

But replacing the current system with pure inflation indexation and a mandatory 30% CGT floor risks creating an even bigger economic problem, because it punishes exactly the kind of long term productive investment the Australian economy depends on.

At a time when Australia already faces weak productivity growth, the last thing we should be doing is discouraging entrepreneurship and long term investment. The real question isn’t whether the current system is perfect. It’s whether Australia can reform capital gains tax without weakening the incentives that drive investment, innovation and economic growth.

I think there’s a fairer and economically smarter middle ground.

Australia became prosperous because people took risks

One of the biggest flaws in the current debate is that it has become framed as a fight between “wealthy investors” and everyone else, which completely misunderstands how productive economies actually work.

Australia became a prosperous country because generations of Australians were willing to delay consumption, take risks, invest capital and build things over long periods of time. Economic growth doesn’t happen automatically. It depends on people being willing to commit their savings toward businesses, housing, infrastructure and productive assets despite uncertainty, volatility and the very real possibility of failure.

That includes the migrant family building a small business over 25 years, the couple slowly investing into ETFs for their children’s education, the regional business owner employing local workers and reinvesting profits back into their company, or the architect, physio or tradesperson spending decades building something valuable rather than maximising short term consumption.

These Australians aren’t speculative traders, or the ‘top end of town’, they’re the backbone of the productive economy.

A healthy tax system should encourage more of this behaviour, not less, because economies become stronger when people believe that if they work hard, invest patiently and build something valuable over time, they’ll still share fairly in the upside they create.

Why inflation indexation creates the wrong incentives

The government’s proposed approach sounds superficially sensible because taxing “real” gains rather than inflationary gains appears fair in theory. But economically, the proposal creates several major problems.

Inflation indexation compensates investors for inflation itself, but it doesn’t properly recognise the enormous uncertainty, opportunity cost and risk involved in long term productive investment. Someone earning interest in a bank account faces relatively little risk, while someone building a business or investing in productive assets could lose everything.

That distinction matters enormously.

Long term investors are locking up already taxed savings for years or decades without any guarantee of success, while also enduring volatility, economic downturns, business failures and changing market conditions along the way. Yet under pure inflation indexation, productive long term investment would often face dramatically higher effective tax rates than it does today.

Over time, that weakens incentives to build businesses, invest in productive assets and commit capital patiently toward long duration growth opportunities.

A country that taxes productive risk taking too heavily eventually gets less of it.

That matters because economies grow when people are willing to delay gratification today in exchange for building something larger tomorrow. If the after tax reward for taking long term risks falls too far, less capital gets invested productively and more gets consumed, parked in low productivity assets or moved offshore.

The Budget proposal also creates a generational divide

One of the least discussed consequences of the proposed changes is the intergenerational unfairness they create, because existing assets are proposed to be grandfathered into the current system while younger Australians inherit a materially worse one.

That means older Australians largely keep the existing tax treatment where they’ve held assets for decades, while younger generations face significantly higher taxes on future investment gains. At a time when younger Australians already feel increasingly locked out of housing and wealth creation, dramatically increasing taxes on long term investment risks deepening that frustration even further.

Good tax policy should bring generations together around long term prosperity, not divide them into winners and losers based purely on timing.

A tapered CGT discount is a fairer compromise

That’s why I believe Australia should consider a tapered capital gains discount instead.

Under this model, investors would receive an additional 5% CGT discount for every year an asset is held, capped at a maximum 50% discount after 10 years. Someone selling after two years would receive a 10% discount, after five years the discount would rise to 25%, and after 10 years the investor would receive the full existing 50% discount.

This creates a much healthier economic incentive structure because short term speculative gains would receive less generous treatment than today and therefore generate more tax revenue, while Australians who spend decades building businesses, funding housing or investing patiently would not suddenly face punitive tax increases.

Most importantly, the system naturally rewards patience, long term thinking and productive capital formation.

Unlike pure inflation indexation, it preserves the idea that long term productive investment deserves different treatment from short term speculation.

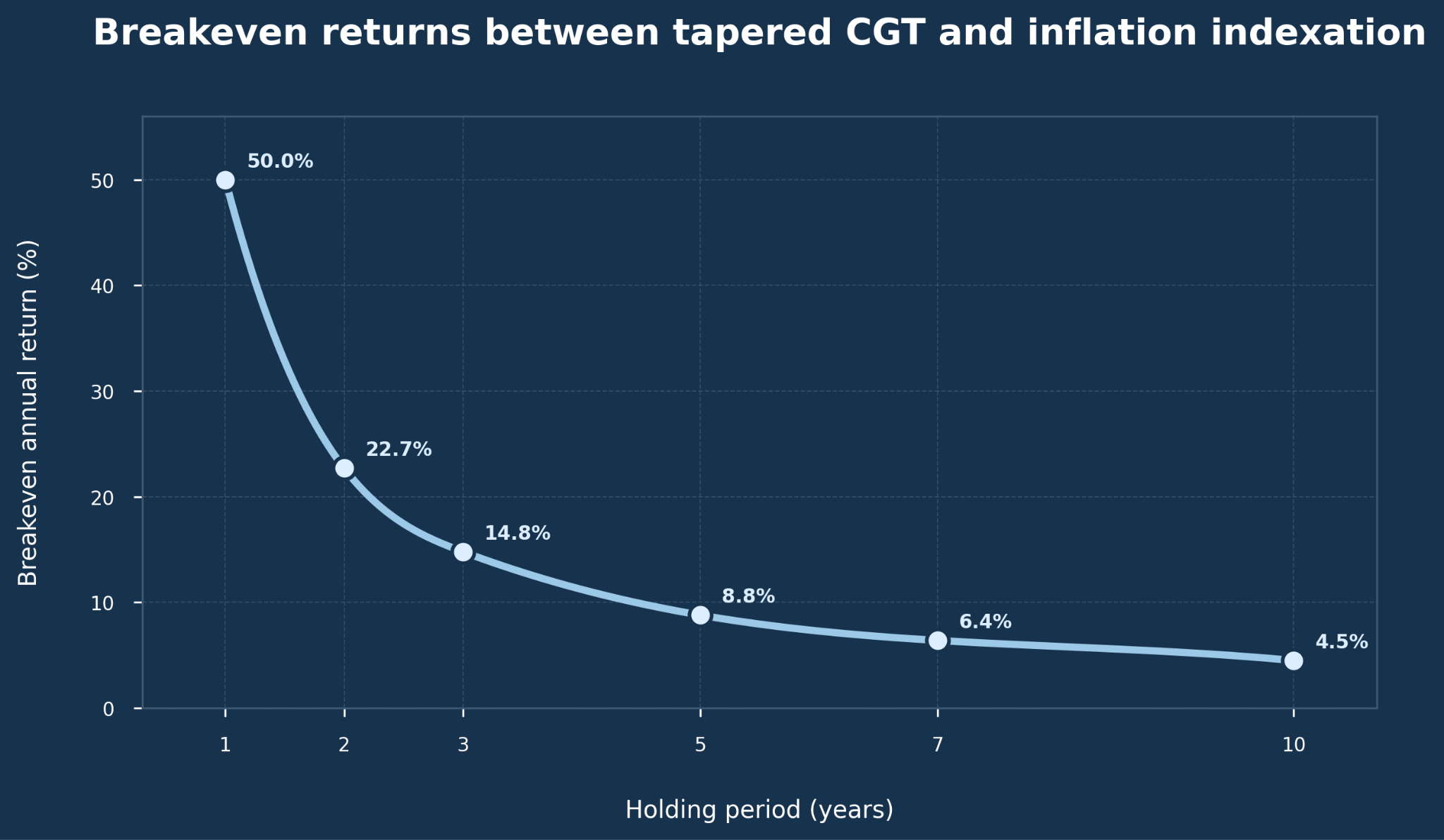

The chart below highlights where the economics of the two systems begin to diverge. It shows the annual investment return at which a tapered CGT discount becomes more favourable than inflation indexation across different holding periods.

| Holding period | CGT discount | Portfolio value | Tax under tapered discount | Tax under inflation indexation | Difference |

| 1 year | 5% | $110,000 | $4,465 | $3,525 | +$940 |

| 2 years | 10% | $121,000 | $8,883 | $7,491 | +$1,392 |

| 3 years | 15% | $133,100 | $13,223 | $11,943 | +$1,280 |

| 4 years | 20% | $146,410 | $17,450 | $16,933 | +$517 |

| 5 years | 25% | $161,051 | $21,520 | $22,518 | -$997 |

| 6 years | 30% | $177,156 | $25,384 | $28,758 | -$3,373 |

| 7 years | 35% | $194,872 | $28,983 | $35,721 | -$6,738 |

| 8 years | 40% | $214,359 | $32,249 | $43,484 | -$11,235 |

| 9 years | 45% | $235,795 | $35,103 | $52,127 | -$17,024 |

| 10 years | 50% | $259,374 | $37,453 | $61,742 | -$24,289 |

| 15 years | 50% | $417,725 | $74,665 | $128,261 | -$53,595 |

| 20 years | 50% | $672,750 | $134,596 | $239,178 | -$104,581 |

The modelling reveals the key economic difference

The really interesting insight from the modelling is that inflation indexation tends to favour lower returning assets, while a tapered CGT discount increasingly rewards investments that generate strong long term real growth.

That’s exactly what good economic policy should do.

Productive assets like businesses and shares have historically delivered returns comfortably above inflation over long periods. For example, Australian shares have generated roughly 6% to 7% annual real returns across decades. Under the tapered model, those productive long term investments continue to receive meaningful encouragement.

By contrast, inflation indexation gradually shifts the tax system toward favouring safer, lower returning and more inflation protected assets, which is the opposite of the incentive structure Australia should want if the goal is stronger productivity, higher wages and long term economic growth.

The modelling below shows the annual investment return at which a tapered CGT discount becomes more favourable than inflation indexation across different holding periods.

The breakeven analysis highlights something economically important. At 10 years, the breakeven nominal return between the two systems is only around 4.5% annually assuming 2.5% inflation, while historically productive growth assets have comfortably exceeded that threshold.

In other words, the tapered system continues rewarding long term productive investment while still reducing overly generous treatment of short term speculative gains.

Economically, that’s a feature rather than a bug.

Australia faces a much bigger economic choice

This debate ultimately isn’t just about tax, it’s about what kind of economy Australia wants to build over the next generation.

Australia already faces weak productivity growth and lower rates of business formation than in previous decades. Now is the worst possible time to weaken incentives for long term productive investment.

A well designed tax system shouldn’t simply maximise next year’s revenue collection. It should shape long term economic behaviour by encouraging Australians to build businesses, invest patiently and commit capital toward growing the economy over decades.

A tapered CGT discount strikes that balance far more effectively, because it still reforms overly generous short term concessions while continuing to reward Australians willing to take risks, build businesses and invest patiently in the country’s future.