To coincide with the release of Scott Pape’s latest book Barefoot Kids (HarperCollins Publishers) Stockspot is republishing this 2018 interview with Scott where he spoke about his books and his well-known investing philosophy.

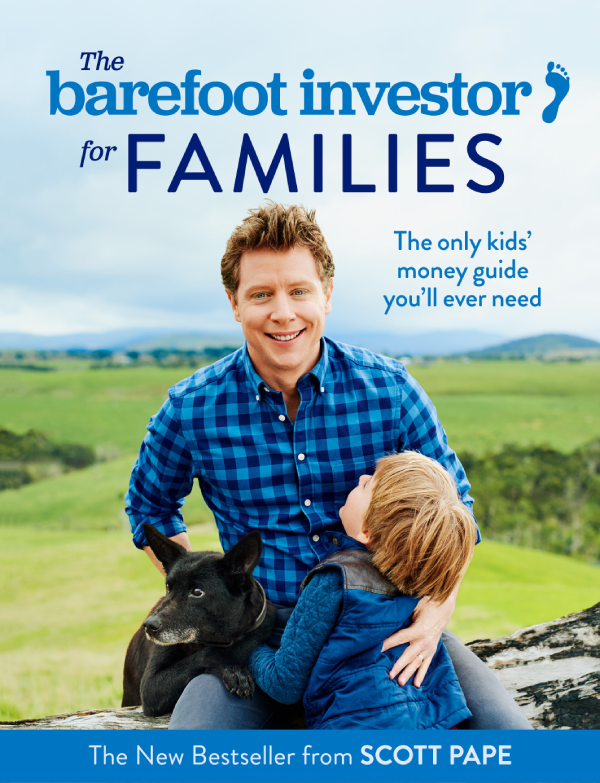

Scott Pape’s The Barefoot Investor for Families is the fastest-selling nonfiction Australian title ever. Straight talking, practical and above all wise, Pape’s Barefoot Investor program for families is part money manual and part good life lessons.

I admit when the book came across my desk I was a little sceptical. However like thousands before me, his approach to money struck a chord. And I don’t even have kids! Scott kindly took some time out of his busy schedule to chat with me about his books and thoughts on money.

You’re one of Australia’s best known and most trusted money celebs, what does that feel like?

I hate the word money celebrity!

My first book The Barefoot Investor, The Only Money Guide You’ll Ever Need, was hailed as an overnight success, the only problem was it took me 15 years of hard work to become an overnight success.

I wrote the book not expecting many people to buy and read it. It totally shocked and surprised me and my publisher when it started selling out. It’s been great and a really wild ride.

I can’t imagine how devastating it was when you lost your family home to the bush fires that ravaged Victoria. How did this experience drive you to write the Barefoot Investor?

I’d been doing Barefoot for over a decade by that stage. It was a time in my life when I had a little baby son, I’d just got married and we literally lost everything that we owned.

We had insurance but it was of those things that was a life changing moment and I realised I had faced a financial fire.

Now I was lucky enough to be in a good financial position where I could say ‘I’ve got this’. I realised that the people who were writing to me (and that I was writing about writing about) faced these financial fire issues.

So I really wanted to write a book that helped people tackle their financial fires, whether that be a divorce, illness, losing their job or just working out how they’re going to pay for their retirement.

I wanted to write it in a way like I was there sitting in a bar with a friend and just telling you how to get your money sorted without a lot of stress.

So why did you decide to write the latest The Barefoot Investor for Families? How is it different from the first?

It was very hard because I wrote the last book as the ‘Only money guide you’ll ever need’.

I’m like the John Farnham finance publishing industry! How do you back that up?

I’ve got three kids under the age of five now, so what I’m really interested in is financial education for young people and kids. I dedicated this book to all the people who read the last book who said why didn’t I get this when I was young?

The book feels part finance and part good life lessons. Was this the intention?

Every parent agrees they want their kids to be financially literate. When I sat down to write the book, I struggled with it and said what does financial literacy actually mean? It’s a terrible term.

I wanted to create a 10 step guide you could do with your kids that if you checked them off by the time they’re adults you’ve done your job. I came up with the Barefoot 10 that you could do with your team (ie your family) practically.

For example the growth of Uber Eats and Deliveroo are being driven by millennials. That’s where the Barefoot 10 comes in with money meals. Sitting down as a family, generally a Sunday night and doing stuff together. That makes a long lasting impression.

You don’t need to give your kids a huge inheritance but if you give your kids those 10 lessons before they leave home your done your job.

So what do you say to the busy parent who feels like life is going full throttle, how can they realistically incorporate these lessons?

I’m a parent and I’m busy so I did this thing for little kids and primary school kids called the 3, 3, 3.

That’s 3 jobs, 3 jam jars that you put your money in and three minutes is all it takes. You do that once a week.

If you can’t find 3 minutes once a week with your kids, well you’re not really trying.

The second one is with the Barefoot 10 which I’ve made into experiences you can have with your kids. I’ve had a lot of people who have done the program and they’ve come back to me and said “this is one of the nicest things I’ve done. It was really fun to do this with my kids and cook dinner with them”.

One of the really great pieces of feedback I’ve had is the $100 challenge. You get your teenagers to go and find a better deal on say your power bill and split the savings with them 50/50. It’s all about building up your kid’s financial confidence.

My mum always bought the home brand versions. It drove me crazy, but now I do the same because it does save money. How important are learned behaviours in shaping our money habits?

The number one predictor of having financially successful and confident kids is to have financially confident parents. That’s why the big thing in my book is all about experiences you can have together.

Everyone says we should learn this in schools and I do kind of agree. However I think there’s an idea that we can outsource all of it to schools, but when you boil it down money is about values and values are taught at home, not at school.

I also think it comes back to that family dinner table and showing your kids how to be an adult rather than sheltering them. If you shelter them and then they come to me when they’re 35 and they’re kidults because they never worked it out.

So like you seeing your mum make savings choices, I grew up watching my parents save for a four bedroom brick veneer home in country Victoria. I watched them for 10 years save for that house and it had an impact.

I love the jam jars. Splurge, Smile, Give. I’m curious as to why the give jar is important?

I surveyed over 10,000 parents before I wrote the book about what’s the biggest concern they have for their kids. The vast majority said the biggest thing that scares them about their kids in terms of finances is their kids will grow up to be entitled brats.

There are only two ways to ensure you don’t have an entitled kid.

One: Get them to work, you don’t work you don’t get paid. No Uber Eats for you!

And two: Give. Show them there are people in their community doing it tough. That it feels good to give. Because we know the tight arses and stingy people are never the happy people. They’re always the people you want to move away from.

The main thing I want for my kids is for them to be generous. I don’t want them to be a pushover, but I want them to have an appreciation for just how good they’ve got it.

In our society we are living through the wealthiest time in human history. And we are fortunate enough to be living in one of the wealthiest countries in history, so it’s very hard to teach them just how good they‘ve got it because have have no perspective on it.

It’s about teaching them to give and learn about people in their community that they can help. It’s not about the money.

What are your thoughts on the FIRE movement? Is it possible?

I think the FIRE movement is great. It packages up the basics of personal finance which are spend less than you earn, save hard and invest the difference.

I do think there are a few unique factors in Australia which make it a bit tougher. If you are living in Balmain it’s going to be very hard to ‘FIRE’ and own a home.

In Australia we have very high house prices which works against the movement. Also I think that as a dad with 3 kids, kids are really expensive!

That said I’m not raining on the FIRE parade.

I think anyone who has a goal for long-term compounding low cost investing I think that’s awesome.

I think for most people who are married, I think FIRE has passed them by. If you’re a young tech person earning great money, then go for it. I just don’t think it works for everybody. To be fair, the FIRE movement would probably argue that as well.

What’s the top of your splurge bucket:

I’m constantly buying stuff for the farm. I’ve got my shearing shed and I attack the Weekly Times [a rural newspaper] like other people attack shopping catalogues. I’m forever splurging on stuff around the farm that really makes no sense.

Stockspot makes it easy to grow your wealth and invest in your future.