Over the past few years, technology has revolutionised how Australians invest. Two of the most popular innovations; micro-investing apps and robo-advisors, have made it easier than ever to grow your wealth without picking stocks or actively managing a portfolio. But while they share some similarities, they serve different purposes and cater to different types of investors.

We have previously compared robo advisers vs financial advisers, what’s the difference between micro-investing and robo-advisors? And which one is right for you? Let’s break it down.

What do micro-investing and robo-advisors have in common?

Both micro-investing and robo-advisors are designed to simplify investing, making it more accessible to everyday Australians. Here’s what they have in common:

Ease of use

Whether you choose micro-investing or a robo-advisor, you don’t need to pick shares or time when to be in or out of the market. These platforms do the heavy lifting for you.

Automated investing

Both options allow you to set up automatic contributions, so you can grow your wealth without having to think about it.

Diversification through ETFs

Instead of investing in individual shares, both micro-investing apps and robo-advisors use exchange-traded funds (ETFs), which spread your investment across multiple assets.

Long-term focus

Unlike trading apps or cryptocurrency platforms, these tools encourage long-term investing to maximise compounding growth.

Key differences between micro-investing and robo-advisors

While they have these similarities, they differ significantly in how they operate and who they’re best suited for.

Minimum investment and top-ups

Micro-investing: Perfect for beginners, micro-investing apps let you start with as little as $5. Many also round up spare change from purchases and invest it for you.

Robo-advisors: Typically require a higher initial deposit, usually around $2,000 to $5,000, allowing for better diversification and lower fees over time. You can start investing with Stockspot with $2,000.

Personalised advice & portfolio management

Micro-investing: These platforms are one-size-fits-all. You can invest, but there’s no personalised financial advice or portfolio structuring based on your needs. Its up to you to pick a portfolio strategy that aligns with your goals.

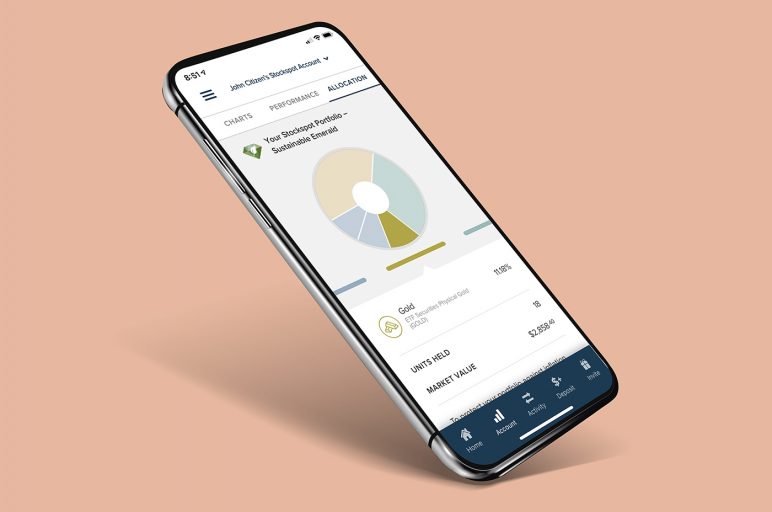

Robo-advisors: Platforms like Stockspot tailor portfolio advice based on your financial goals, risk tolerance, and investment timeline.

Learn more about how personalised investment advice helps you invest better here.

Ownership structure: HIN vs. custodial

Micro-investing: Most platforms use a custodial model, meaning you don’t directly own the shares or ETFs in your name. Instead, you hold ‘units’ in a pooled trust. This means that if you ever leave, you’ll need to sell your portfolio and realise capital gains (and potentially pay tax).

Robo-advisors: Stockspot uses a Holder Identification Number (HIN) structure. This means the ETFs in your portfolio are owned in your name, providing greater transparency, control, safety and potentially tax efficiency.

Learn more on custody vs HIN here.

Which investment option is right for you?

Micro-investing might be right if:

- You’re just starting out and want to invest small amounts.

- You’re looking for an easy way to get into the habit of investing.

- You’re comfortable with limited investment choices and a custodial ownership structure.

Robo-advisors might be right if:

- You’re ready to build long-term wealth with a structured portfolio.

- You want personalised investment advice tailored to your financial situation.

- You prefer direct ownership of ETFs (HIN structure) for better safety, transparency and control.

- You want an optimised, tax-efficient investment strategy.

Helping Australians build long term wealth

Many Australians start with micro-investing and later transition to a robo-advisor like Stockspot as they build wealth and seek a smarter, more cost-effective strategy. While micro-investing is great for dipping your toes into investing, robo-advisors provide a more comprehensive and optimised approach for long-term success.

At Stockspot, we’ve been helping Australians invest smarter since 2014. Our portfolios are designed for diversification, risk management, and tax efficiency, giving you the best chance of growing your wealth over time.

Learn how Stockspot outperformed Vanguard and other robo advisers here.