The government says its proposed capital gains tax reforms are designed to make the tax system fairer and improve housing affordability. However, buried inside the new framework is a major unintended consequence that Treasury’s modelling may understate.

The proposed system could heavily favour ETF investing and other pooled structures like LICs over holding diversified portfolios of individual shares. The issue comes down to how the new system treats gains and losses relative to inflation and, ironically, the more diversified your direct share portfolio is, the worse the problem can become.

In this article, I’ll break down why the proposed framework particularly disadvantages portfolios with a high dispersion between winners and losers, which is exactly how many long term share portfolios behave. This issue was first raised in the AFR article “Investors face 50pc more tax than Treasury says”.

This is a significant problem because according to the latest ASX Investor Study, 7.7 million Australians invest in listed securities outside super, many of whom hold direct shares.

How the current system works

Under the current 50% CGT discount model, investors pay tax on nominal capital gains and can offset nominal capital losses against those gains.

Importantly, the system treats gains and losses symmetrically.

If one share rises by $100,000 and another falls by $100,000, they broadly offset each other regardless of inflation. Investors are effectively taxed on their net nominal gain across the portfolio.

That means diversified portfolios behave pretty intuitively under the current framework. Some investments outperform, some underperform but over time the gains and losses naturally net off against each other.

The maths of investing

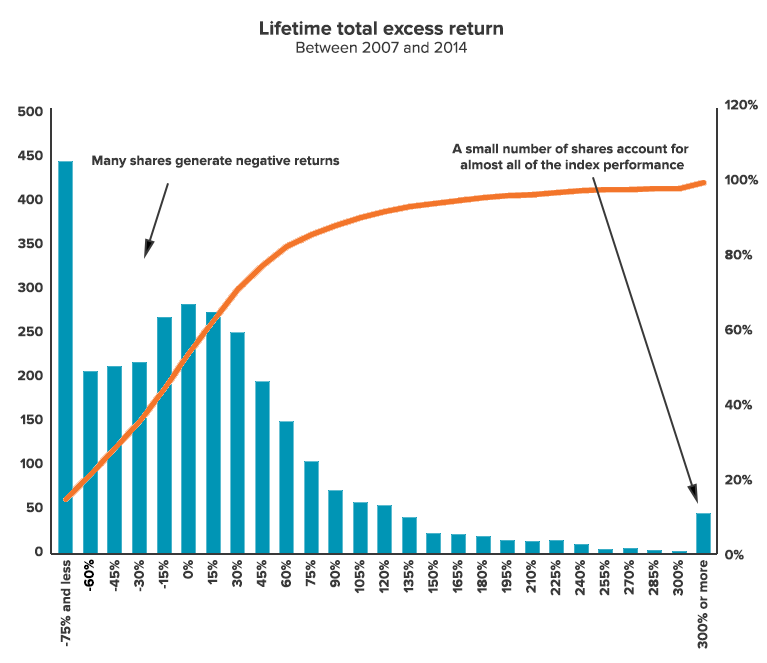

One of the most surprising realities of sharemarket investing is that most individual shares actually underperform the market index over long periods.

Research from J.P. Morgan found the median stock in the Russell 3000 underperformed the broader index by almost 100 percentage points between 1980 and 2014.

In fact, around two thirds of stocks underperformed the broader market. Less than 7% of companies generated most of the overall market returns.

That means long term sharemarket returns are heavily driven by a very small number of extreme winners.

This fact matters a lot here because diversified portfolios naturally contain a small number of extreme winners alongside many mediocre or underperforming investments.

Under the current 50% discount system, those outcomes broadly offset each other over time.

Under the proposed indexing model, they no longer do.

How the proposed indexing model changes everything

Assume an investor builds a diversified direct share portfolio with four equal investments of $10,000 each over 20 years.

There four shares are across different market sectors and the portfolio behaves much more like real world long term share investing: One extreme winner increases by 10x, two shares rise modestly in nominal terms but still underperform inflation, one investment fails completely and goes to zero.

Assume inflation averages 3.5% over the period, meaning the inflation adjusted cost base roughly doubles over the 20 years. Economically, the portfolio only generates a moderate real gain overall after inflation. But tax is calculated investment by investment rather than across the true real economic outcome of the overall portfolio.

| Investment | Final value | Nominal gain/(loss) | Inflation adjusted cost base | Real gain/(loss) after inflation | Tax treatment under current 50% CGT discount | Tax treatment under proposed indexing model |

| $10,000 (share 1, extreme winner) | $100,000 | +$90,000 12.2% p.a. | $20,000 | +$80,000 8.4% p.a. | $90,000 nominal gain taxed at 50% discount | $80,000 taxable real gain |

| $10,000 (share 2, mediocre performer) | $14,800 | +$4,800 2.0% p.a. | $20,000 | -$5,200 -2.0% p.a. | $4,800 nominal gain taxed at 50% discount | No usable offset |

| $10,000 (share 3, mediocre performer) | $12,200 | +$2,200 1.0% p.a. | $20,000 | -$7,800 -2.5% p.a. | $2,200 nominal gain taxed at 50% discount | No usable offset |

| $10,000 (share 4, failed investment) | $0 | -$10,000 -100% | $20,000 | -$20,000 -100% | Full $10,000 nominal capital loss offset available | Only nominal $10,000 loss recognised |

| $40,000 (bombined portfolio) | $127,000 | +$87,000 ~6.0% p.a. | $80,000 | +$47,000 ~2.4% p.a. | Gains and losses broadly offset in nominal terms | Tax overwhelmingly driven by the 10x winner |

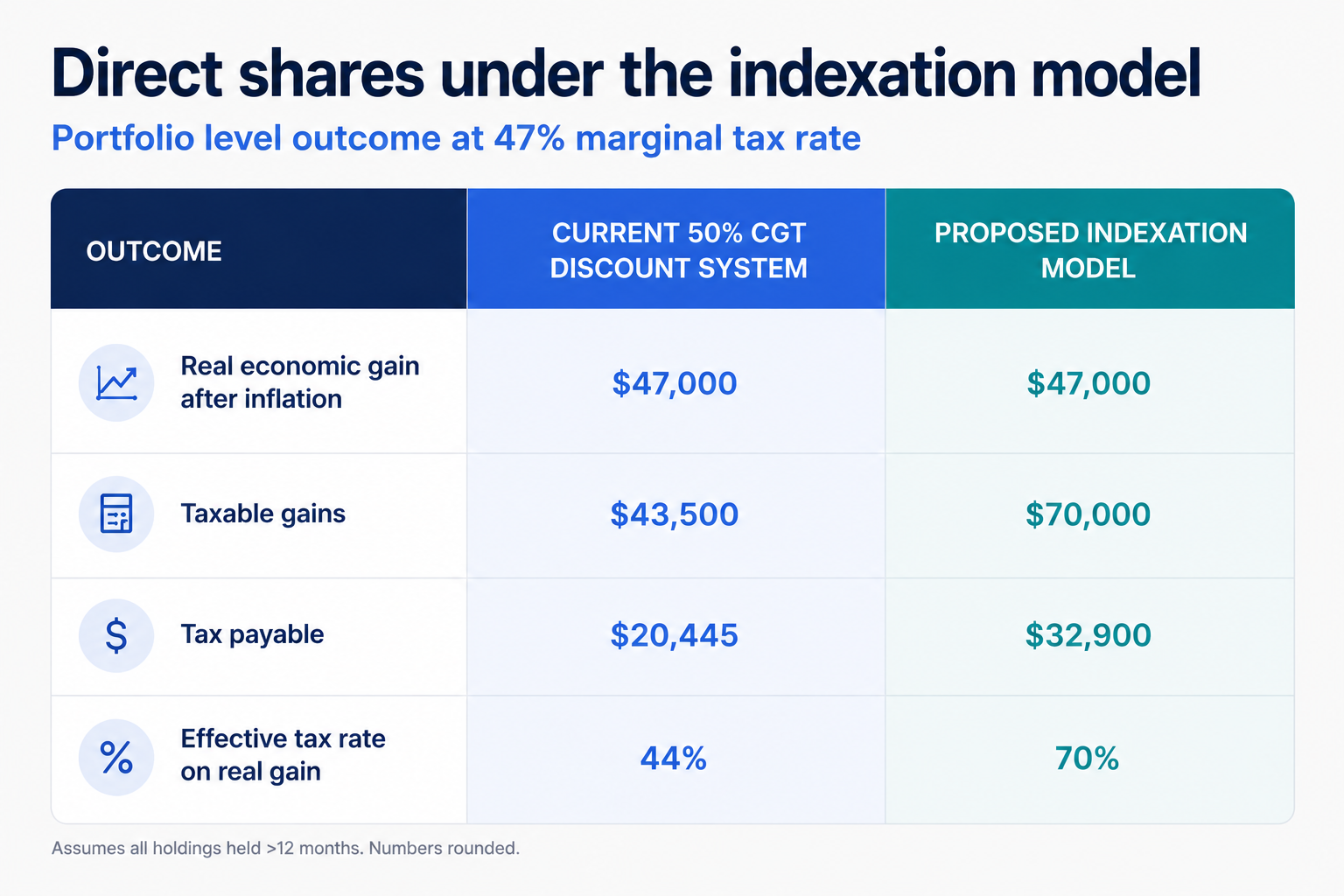

Tax comparison for direct shares

Importantly, the effective tax rates below are measured relative to the investor’s true inflation adjusted purchasing power gain, not their nominal gain.

The investor only made a real gain of roughly $47,000 across the entire portfolio after inflation.

But under the proposed indexing system, the inflation adjusted underperformance of shares 2 and 3 is largely ignored because those shares still rose slightly in nominal dollar terms. Meanwhile, only the nominal decline in share 4 can offset gains, not the much larger real economic loss after inflation.

As a result, tax is driven overwhelmingly by the one major winner in the portfolio.

The investor ends up paying almost $32,900 in tax despite only generating a real economic gain of roughly $47,000 across the entire portfolio.

Treasury’s modelling may be broadly accurate for broad market index investing, but it’s much less representative for diversified portfolios of individual shares because of this dispersion of returns.

Why ETFs are treated much more favourably

This issue is much less severe inside broad index ETFs.

That’s because ETFs effectively pool winners and losers internally. Underperforming companies gradually leave the index over time while successful companies become larger weights. Gains and losses are smoothed across the structure and investors are generally only taxed when they sell the ETF itself.

Broad diversified ETFs are generally less exposed because they behave more like a single compounding investment over time.

However, the same issue may still affect more volatile thematic or sector ETFs where long term returns are less stable or where portfolios experience larger swings between winners and losers.

As a result, Treasury’s modelling works reasonably well for broad market ETFs because the ETF behaves more like a single compounding investment.

But that same modelling becomes much less representative for diversified portfolios of individual shares.

Former Treasury official Geoff Francis explained the issue clearly in the AFR this week:

“You will typically pay more tax than the Treasury numbers suggest because the only way you get the Treasury numbers is if you invest in an indexing tracking stock.”

Why this matters for Australians with direct shares

This issue particularly affects Australians building wealth outside super using direct share portfolios and people investing into startups, small caps and emerging companies.

Perhaps unintentionally, the proposed system may end up pushing Australians toward indexed broad market index ETFs, other pooled structures like LICs and managed funds and super while discouraging direct ownership of ASX listed companies, entrepreneurial investing and higher risk long term capital formation.

It may prove to be one of the most economically significant unintended consequences of the proposed reforms.