Starting a pension doesn’t need to be complicated.

Many Australians searching “how do I start a pension?” or “move super to retirement income” are unsure where to begin or what steps are involved.

Stockspot Pension is designed to make the process clear and straightforward, helping you move from superannuation to retirement income in a simple and supported way.

What you need before you start your Stockspot Pension

Before starting your Stockspot Pension, it helps to have:

- Your Tax File Number (TFN)

- A valid form of identification

- Details of your current super fund

You’ll also need to confirm whether you’re still working or fully retired, as this determines the type of pension account that applies and your eligibility to start drawing a pension.

How do you choose the right pension account?

Stockspot supports the two most common pension types used in Australia.

- Transition to Retirement (TTR) pension

If you’re still working, a TTR pension may allow limited income withdrawals while your super remains invested. Specific withdrawal limits and tax rules apply.

- Retirement Income pension

If you’ve retired, a Retirement Income pension generally provides more flexibility in how income is paid. For most Australians aged 60 and over, earnings and withdrawals are tax-free.

During setup, Stockspot guides you through this choice and applies the appropriate structure for you.

How do you roll over your super to Stockspot Pension?

When you set up your account, you will need to tell us which super funds you would like to roll in.

Your super rollover is then completed securely online.

Once your super balance is received by Stockspot:

- Your pension portfolio is invested

- Your pension account is formally commenced

- Your income payments are scheduled and your selected intervals

You’ll receive confirmation of your pension start date and payment details once the process is complete.

How to nominate beneficiaries

As part of the setup process, you can nominate beneficiaries to receive your pension balance if you pass away. Options include:

Reversionary beneficiaries: commonly a spouse

This passes the pension automatically to a spouse or dependent on death

Preferred beneficiaries: which guide trustee decisions

This is a non-binding nomination and acts as guidance to a trustee

Binding beneficiaries: which are legally enforceable

This is an enforceable direction

Stockspot explains each option clearly so you can choose what aligns with your circumstances.

How to set up your pension income payments

Choose how often you’d like to receive income from your pension, this can be:

- Monthly

- Quarterly

- Annually

Your nominated income amount must meet minimum pension rules, and you can update your payment preferences at any time through your online dashboard.

What happens after your pension starts?

Once your Stockspot Pension is active, your dashboard provides visibility of:

- Income payments

- Portfolio performance

- Account and pension details

Everything is available in one place, helping you stay informed without additional administration.

How Stockspot support you throughout the pension process

If you need help at any stage, Stockspot’s Australian-based client care and support team is available to assist with:

- Super rollovers

- Beneficiary nominations

- Income payment changes

Support is available both before and after your pension begins.

Starting a pension is an important step. Stockspot aims to make it clear, structured and well supported.

Pension FAQs

What is a pension account in Australia?

A pension account allows Australians to convert their superannuation balance into a retirement income stream, while keeping the balance invested in pension phase under Australian superannuation rules.

How does a pension work once I retire?

Once you retire, your super balance moves into pension phase. You can draw regular income payments while your remaining balance stays invested, with earnings generally tax-free under current legislation.

What is the difference between super and a pension?

Superannuation is used to accumulate savings while you’re working. A pension is used to draw income in retirement from your super balance, subject to minimum withdrawal rules.

What is a Transition to Retirement (TTR) pension?

A Transition to Retirement pension is designed for Australians who are still working but want limited access to their super. Withdrawals are capped, and specific tax rules apply.

When can I start a retirement income pension?

Most Australians can start a retirement income pension once they reach their preservation age (which depends on their birth year) and meet a condition of release, such as retirement.

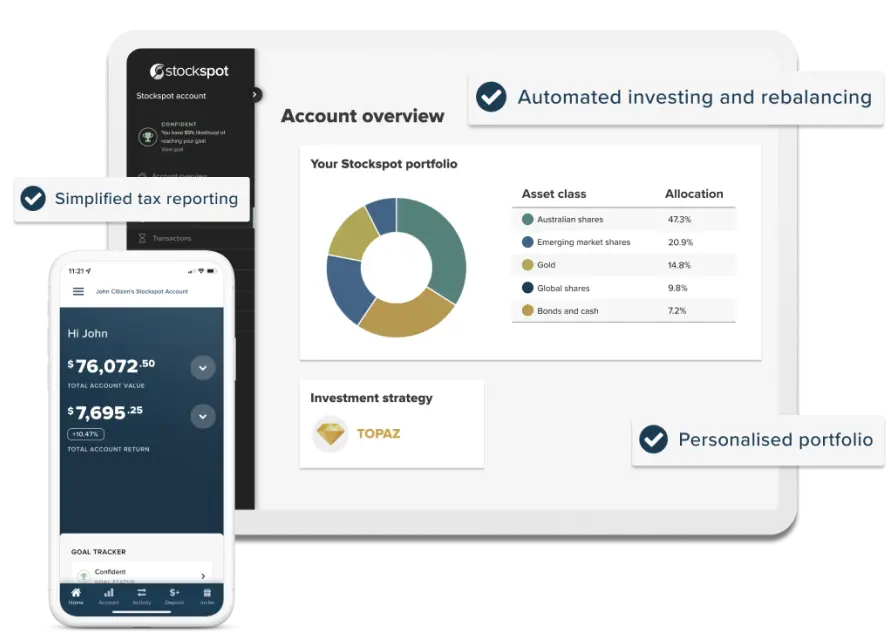

How is a Stockspot Pension invested?

Stockspot Pension portfolios are invested in exchange traded funds (ETFs), providing diversified exposure across asset classes and markets.